Global Plant-Based Sales Up By 5% in 2024 Despite US Setback: New Report

The Good Food Institute, an alternative protein think tank, has released its latest State of the Industry series of reports for 2024. Here’s how plant-based, fermentation-derived and cultivated proteins fared in 2024.

While investment in alternative protein continued to fall in 2024, global sales of plant-based meat and dairy alternatives are up, as is interest in whole foods, according to the 2024 State of the Industry reports by industry think tank the Good Food Institute (GFI).

The annual series of reports explores the challenges and opportunities for plant-based food, fermentation-derived proteins, and cultivated meat. This year’s editions reveal a complex landscape for alternative proteins, with sales in markets like the US still declining and public investment in the industry on the rise.

Alternative proteins are part of a polarising debate in many parts of the world, punctuated by high prices and taste concerns, and enveloped by the backlash against ultra-processed foods (UPFs). However, the global performance shows promise in the market at a time when it has been portrayed as anything but.

Global plant-based sales on the rise

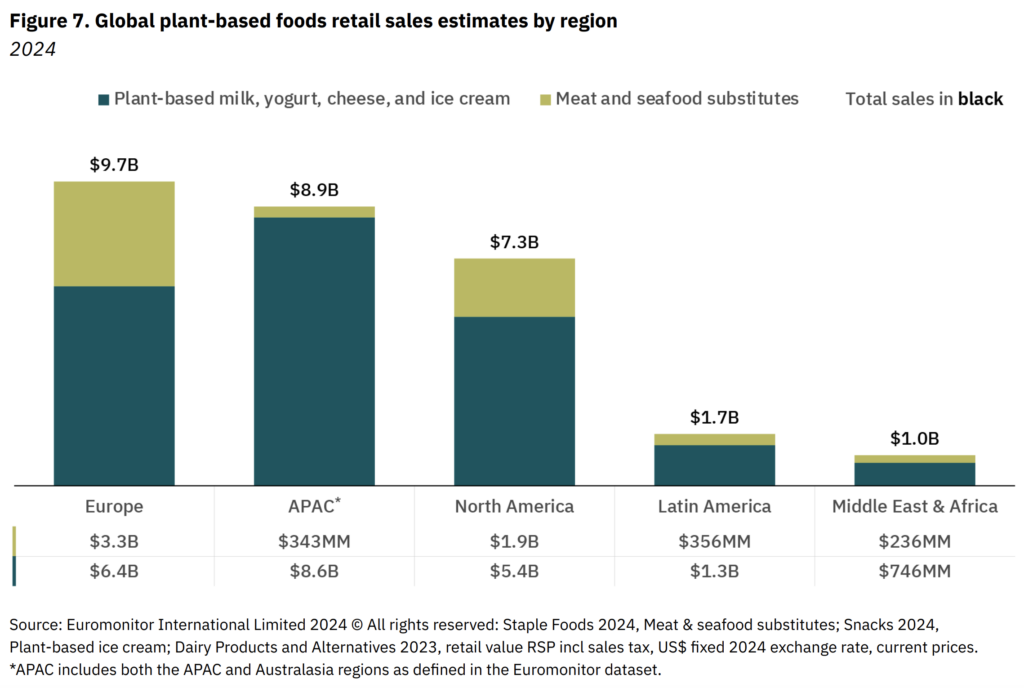

You’d be forgiven for thinking that sales of plant-based foods took a giant plunge, given all the coverage and discourse around them. In actuality, global sales reached $28.6B, a 5% increase from 2023.

Non-dairy alternatives dominated the market, with sales up by 5% to reach $22.4B, while meat analogues hit $6.1B (a 4% increase). After milk, meat and seafood, vegan yoghurt is the most popular category.

Europe was the leader in 2024, recording $9.7B in sales of plant-based meat, seafood and dairy, followed by Asia-Pacific ($8.9B), and North America ($7.3B), where conventional beef sales reached a record high last year.

Meat and dairy alternatives decline in the US, while whole foods shine

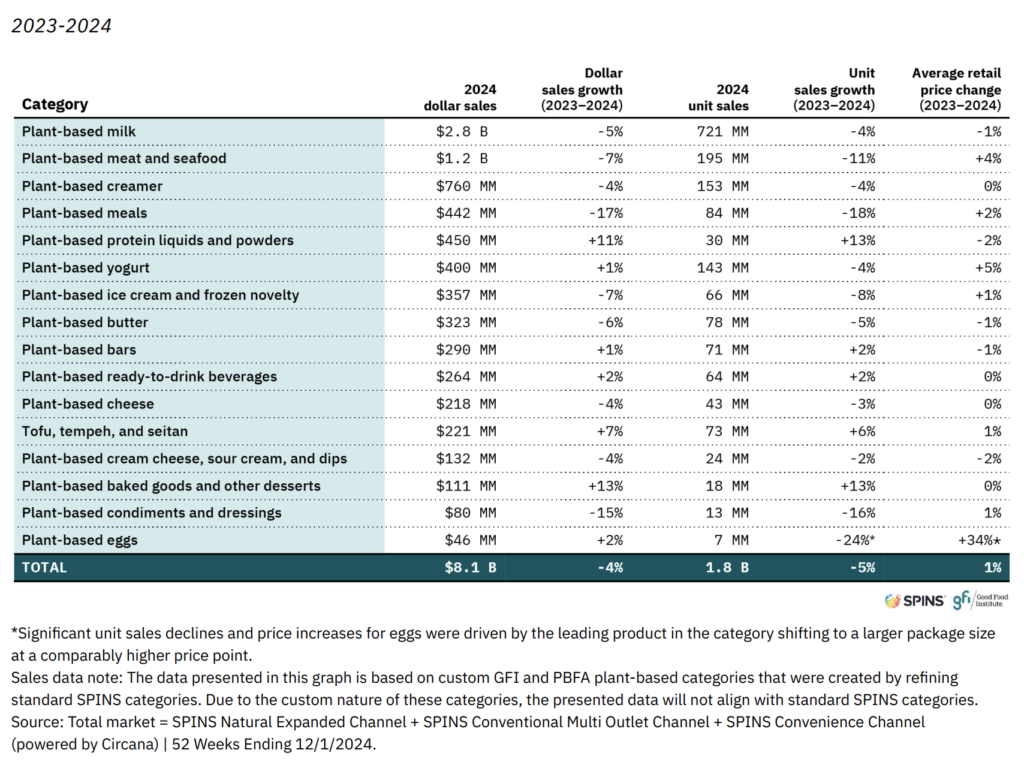

In the US, overall plant-based sales reached $8.1B in 2024, a 4% decline from 2023. More than a third of the market (34%) was occupied by non-dairy milk alone, whose sales dropped by 5% to $2.8B. Likewise, meat and seafood alternatives saw dollar sales fall by 7% to $1.2B, though the rate of decline was slower than in 2023.

At the same time, the demand for protein led to an increase in sales of protein powders (11%), and growing interest in whole foods resulted in a 7% hike in sales for tofu, tempeh and seitan. The biggest windfall, however, came for vegan desserts and baked goods (13%).

Plant-based eggs, meanwhile, saw a 2% increase in retail sales as avian flu wrecked chicken egg supplies in the US. This was true for foodservice too, where vegan egg sales were up by 28%. The report authors note that the data on unit sales and price changes is somewhat skewed due to the leading product in the category shifting to a larger pack size and thus a comparably higher price point.

Still in foodservice, plant-based proteins suffered a 5% decline in sales, though non-dairy milk continued its climb with a 9% growth.

Price parity and consumer reach still hindrance for the plant-based sector

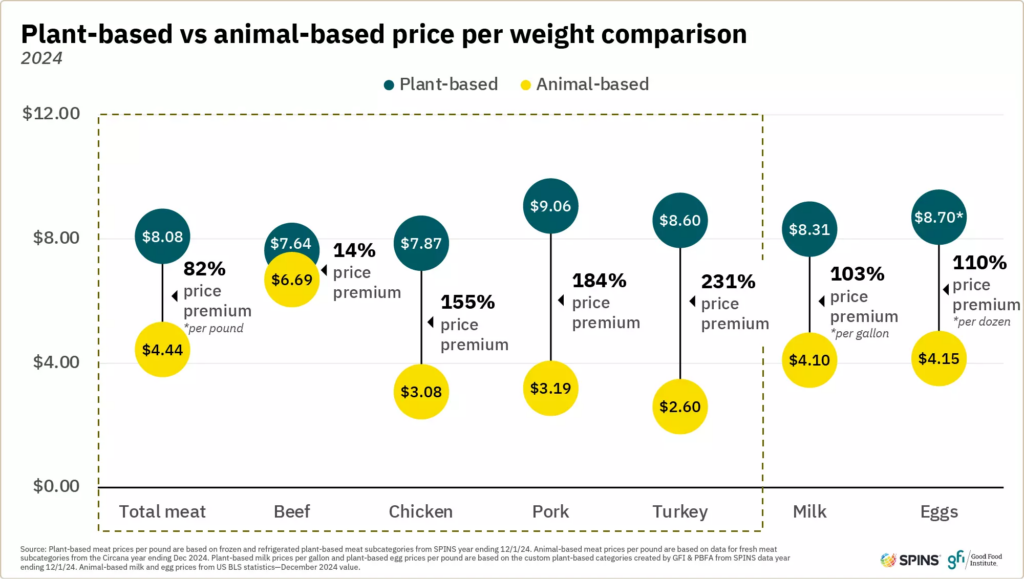

Plant-based meat and seafood were 4% more expensive in 2024, versus just a 1% price hike for their conventional counterparts, widening the former’s premium to 82%.

The price gap for chicken and milk remained the same, while widening for pork and turkey. On the flip side, rising beef rates mean plant-based versions are just 14% more expensive now. And chicken-free eggs, which had a 317% price premium in 2023, narrowed this to 110%.

Bringing down prices of plant-based food is critical for them to compete with animal-derived products, as is improving consumer reach and acceptance. In the US, 59% of households bought a vegan product in 2024, similar to the year before, though down from 63% in 2022.

Penetration of plant-based meat and seafood remains low at 13%, though encouragingly, 63% go back to the store for more. Further, almost all Americans who buy these alternatives are not vegan or vegetarian – 96% of buyers also put conventional meat in their shopping baskets in 2024.

Milk alternatives reached 40% of households, with a repeat rate of 76%. Almond milk continues to remain the most popular dairy alternative (capturing 54% of sales), but oat milk is on the rise (25%).

VC investment slides, public funding a bright spot

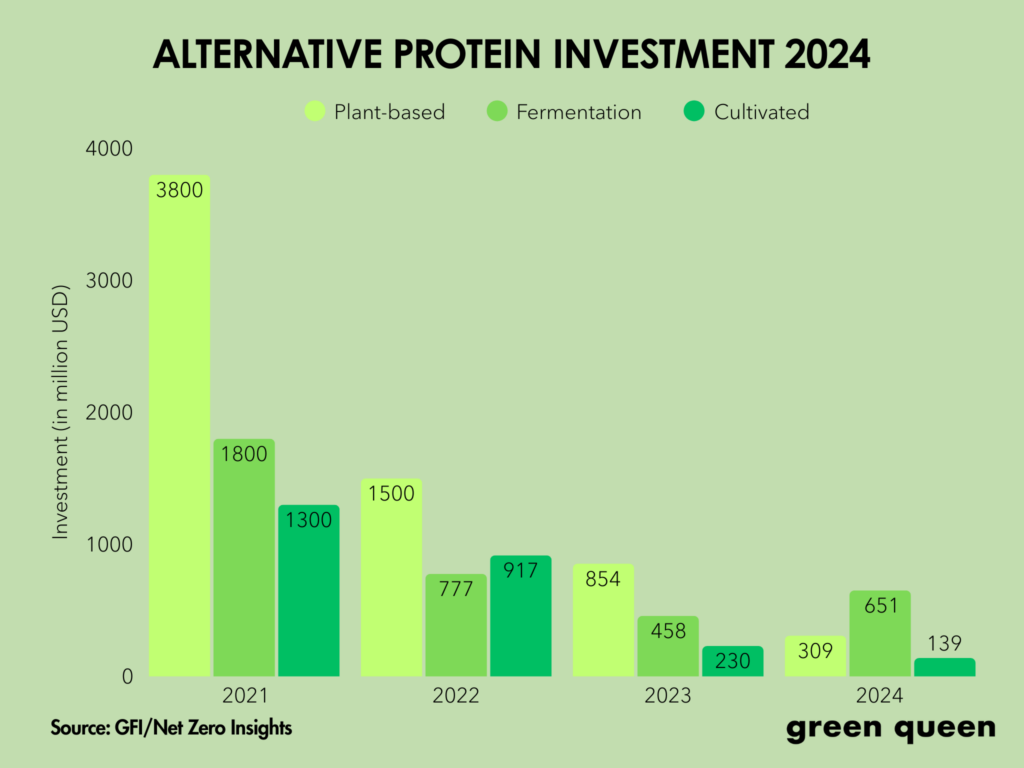

Alternative proteins did not escape the bleak landscape for climate tech venture capital in 2024, with total funding for the sector only amounting to $1.1B, a 27% decline from the year before.

Plant-based companies took the biggest hit, as venture capitalists backed away from foods linked to ultra-processing. These startups only raised $309M in 2024, a sharp 64% fall from the year before.

Cultivated meat, meanwhile, witnessed a 40% decline, securing only $139M, its lowest annual total since 2019. In fact, in the last three years, this sector has cumulatively raised less money than it did in 2021 alone.

The only bright spot for the category here is fermentation, where VC investment experienced a 43% increase last year, overturning a decline in 2023. This was led by Meati‘s $100M Series C round. Further, this category surpassed plant proteins in terms of the amount of public capital invested.

Speaking of which, while private investors remained cautious, governments continued to pour money into alternative protein, amid a push to meet their net-zero goals and mounting pressure from climate experts to diversify protein sources. Public investment in alternative proteins reached $510M in 2024, in line with the year before.

This was driven by the US, Denmark and the EU overall, while Asia-Pacific played a major role in the doubling of public funding for cultivated meat in 2024.

Legislative headwinds make for uneven regulatory progress

2024 was a milestone year for companies making novel food from precision, biomass and gas fermentation, with several regulators greenlighting products like cow-free casein, CO2-derived protein, and animal-free egg protein.

However, in the US, Robert F Kennedy Jr’s potential removal of the self-affirmed Generally Recognized as Safe (GRAS) pathway could stall this momentum.

Meanwhile, cultivated meat continues to face threats of bans in the US and elsewhere. According to GFI’s calculations, 12 states attempted to restrict cultivated meat last year, with Florida and Alabama being successful – the former is now facing a lawsuit from California’s Upside Foods. Already this year, a host of other states have proposed similar bills, with Mississippi becoming the third to enact a ban.

Even so, cultivated meat regulation progressed in several other markets in 2024. Australia’s Vow was cleared to sell its cultivated quail and foie gras in Singapore (and later in Australia and New Zealand), and UK’s Meatly earned UK approval to commercialise cultivated chicken for pets, following Aleph Farms‘s greenlight in Israel in December 2023. Plus, regulators in the EU, South Korea, and Thailand received their first applications.

“Although some uncertainty exists due to shifting political winds around the globe, more approvals are likely in 2025,” said GFI. “These approvals will increase the number of cultivated meat products on the market while also generating new and more robust data on their safety and nutritional profile”