What Do 2025’s Investment Trends So Far Tell Us About Alternative Proteins?

After a decline in alternative protein investments in 2024, funding further fell by 28% in Q1 2025 compared to the same period a year ago. Analysts blame AI, high costs, and low sales.

There’s no other way to put it: 2024 was a bleak year for food tech. Post-Covid geopolitical tensions and higher living costs continued to threaten both shoppers’ wallets and investor sentiment, and startups aiming to futureproof the food system bore the brunt of the impact.

It hasn’t gotten any easier, with 2025 bringing its own set of headwinds. President Donald Trump’s tariff war, Robert F Kennedy Jr’s attack on ultra-processed food and regulatory pathways, more bans on cultivated meat, a resurgence of beef and dairy both stateside and in Europe, and continued sales declines in several markets have all contributed to the storm engulfing the alternative protein industry.

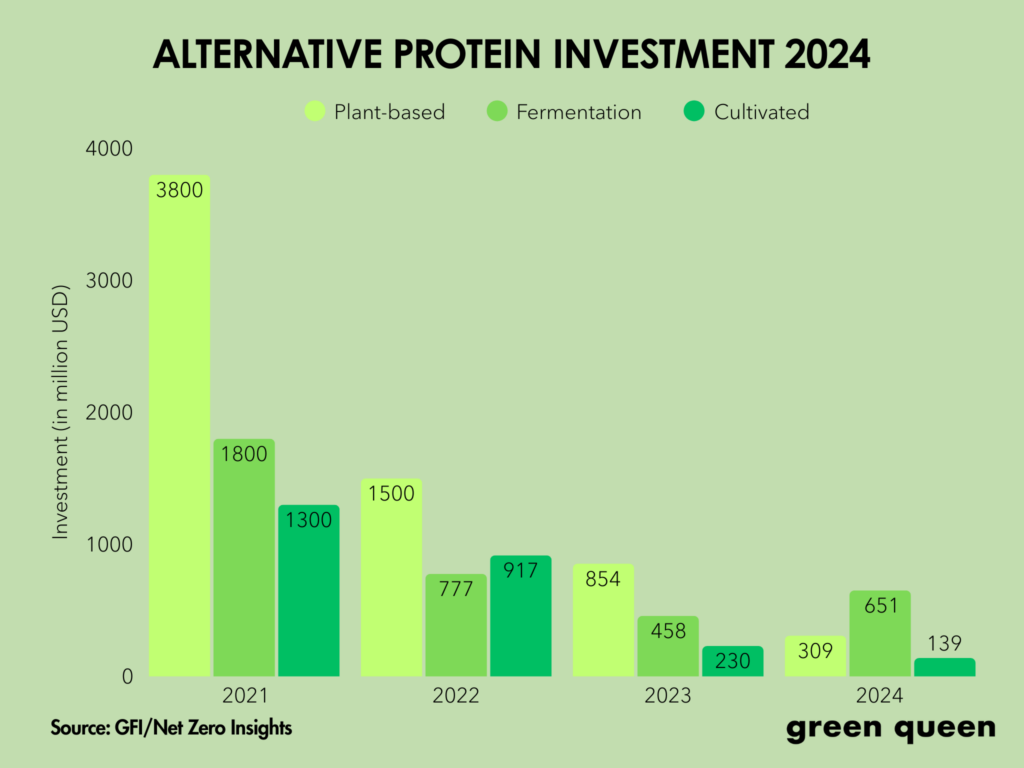

After a 44% drop in 2023, VC investments in plant-based food, fermentation-derived ingredients, and cultivated meat fell by a further 27% in 2024, according to Net Zero Insights data crunched by the Good Food Institute (GFI)

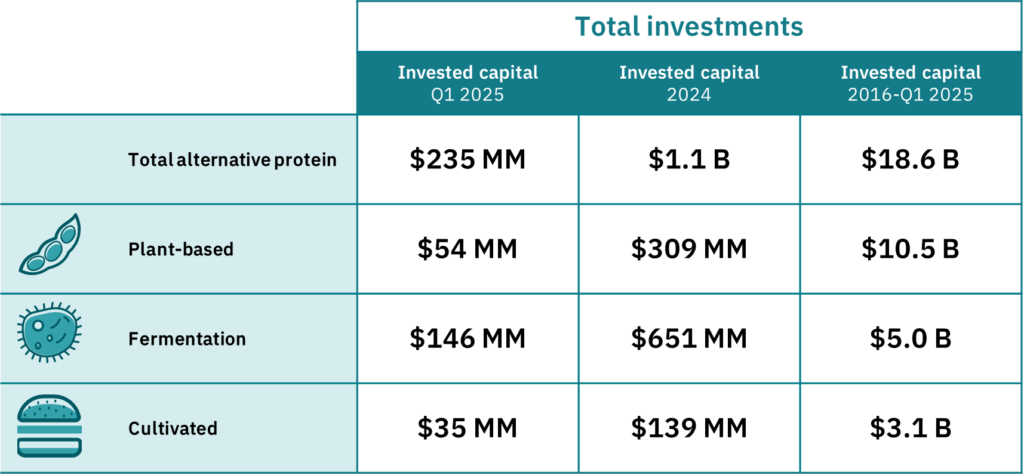

Q1 2025 investments in the sector declined by 28% YoY, falling to $235M. Fermentation startups capture the bulk of this, attracting $146M, while plant-based ($54M) and cultivated protein firms ($35M) continued to falter.

So who – or what – is to blame? And are there any bright spots for alternative protein?

Fermentation continues to thrive

Looking at the figures for both 2024 and early 2025, one segment sticks out: fermentation. It was the only alternative protein pillar to witness an increase in investment last year (by 43%), against decreases for both plant-based food (-64%) and cultivated meat (-40%).

In Q1 2025, fermentation startups attracted half of all funding flowing into the sector, with precision fermentation particularly piquing investor interest. This tech vertical was responsible for the three largest rounds of the quarter: Formo’s $36M venture debt loan from the European Investment Bank, Vivici’s $33.8M Series A round, and Liberation Labs’s $31.5M investment.

The only other investment round above $25M in this period was for Israeli cultivated meat startup Aleph Farms, which secured $29M as part of a larger fundraise in the coming months.

“Many of the fermentation companies that received large investments are focused on leveraging agricultural and food industry sidestreams as a sustainable feed source, helping produce food more efficiently and affordably – both of which are attractive propositions for investors,” Helene Grosshans, infrastructure investment manager at GFI Europe, wrote last year about the success of fermentation.

Still, fermentation investment totals fell year-over-year in Q1 2025, according to Daniel Gertner, lead economic and industry analyst for the organisation, yet ranked in the top half of the 10 most recent quarters.

So while alternative protein funding remained subdued in the first quarter of this year, he warns that “few meaningful trends can be identified in a single quarter”.

Can Europe keep up its momentum?

Alongside fermentation, European startups showed promising signs, collectively raising $509M in 2024 (a 23% annual increase). This included a record year for Germany, where alternative protein firms attracted $145M (although $61M of that came from Formo’s Series B round).

Here, too, fermentation shone. Biomass fermentation startups saw a 10% hike in investment in 2024, while those working on precision fermentation bagged more than thrice the funding totals of 2023. As mentioned above, that trend has continued this year, thanks to Vivici and Formo’s latest rounds.

While at first glance it may seem that plant-based and cultivated meat startups performed miserably, context is crucial. As GFI Europe’s Grosshans points out, the decline for the former category is due to Oatly’s large $425M raise over two deals; if you discount publicly traded companies, privately held plant-based firms in Europe actually saw investment grow by 37% last year.

Similarly, two relatively large deals for Mosa Meat and Meatable, totalling $53.3M, skewed the data for cultivated meat, too, where funding dipped by 59%. These two Dutch startups are preparing to enter the market soon, so they’re not reflective of where most of the sector is.

AI has wrecked the investment landscape for everyone else

In 2024, there was a 38% dip in climate tech venture funding, thanks to a shift in investor interest towards artificial intelligence (AI), where financing crossed $100B.

In the first 12 weeks of this year, AI propelled global venture financing to its highest quarterly levels in nearly three years. OpenAI, the maker of ChatGPT, raised $40B – that’s with a ‘B’ – which led AI to account for 58% of VC deal value in Q1 2025.

Non-AI sectors, however, experienced their weakest deal activity in a decade, notes Gertner. “Recent growth in overall venture funding has largely been driven by surges in AI investments, which have likely redirected capital flows from other industries,” he tells Green Queen.

“Alternative protein funding has slowed amid this increased investor focus on AI, while elevated interest rates, high production costs, and topline sales declines have also weighed on investment activity,” he adds. “Alternative proteins are not alone in this trend: adjacent industries like climate tech and consumer packaged goods have experienced similar investment slowdowns.”

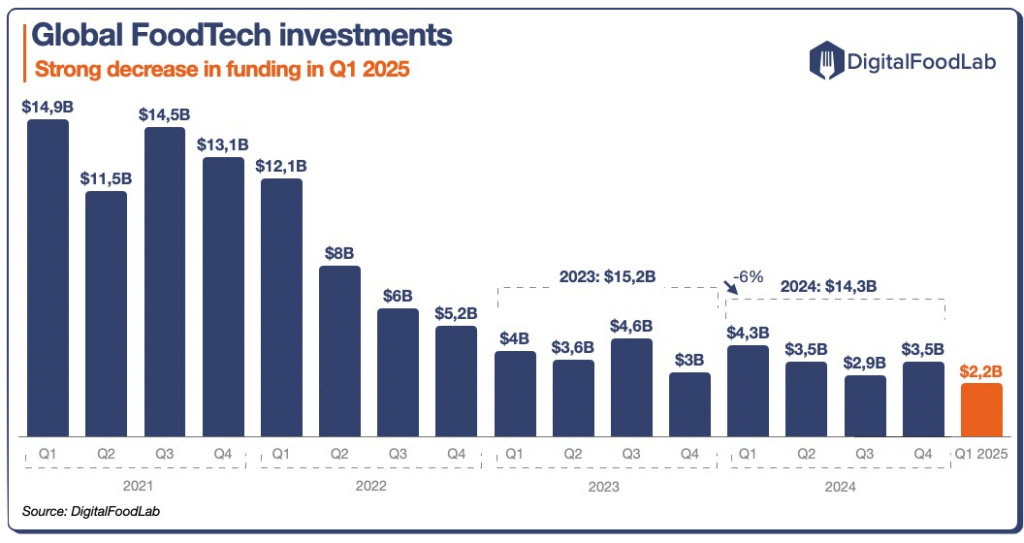

Indeed, the wider food tech sector’s $2.2B funding in Q1 2025 was the worst quarterly performance in years. Matthieu Vincent, co-founder of strategy consultancy firm DigitalFoodLab, ascribes this to contextual reasons, as opposed to structural factors like the VC ecosystem being unsuited to long-term innovation.

The Q1 decline is linked to “the current economic uncertainties, notably on tariffs and their impact on the overall agrifood industries”, he explained in his newsletter.

Trump’s tariffs have already had investors worried, with Grey Silo Ventures’s investment manager, Matteo Leonardi, telling Green Queen last month: “As we are dealing with an industry that is already fighting to survive on the slightest of margins – and at industrial scale, let alone at pilot scale – US tariffs could result in a complete erosion of those already-thin margins.”

Adam Bergman, managing director of EcoTech Capital, predicted the downturn to continue in 2026. “I expect that over 70% of agtech and food tech companies will either go bankrupt, cease operations, or be liquidated in a fire sale. It is likely that a similar percentage of the capital invested in these companies will never be recouped,” he wrote.

The way forward for alternative protein

“As AI dominates investor attention, alternative protein companies are either developing novel applications of AI for alternative proteins or choosing to compete for a smaller slice of non-AI capital,” Gertner wrote in a recent newsletter, signalling the pivots this sector may need to make to survive.

Leading companies also need to turn their sales around, and fast. Addressing misinformation about meat, dairy, and plant-based alternatives is a crucial step.

“Instead of creating more noise, we have been systematically engaging with registered and renowned dietitians, nutritionists and key opinion leaders, arming them with science-based facts about our category and our products, so they can be advocates for the truth,” said Daniel Ordonez, COO of Oatly, which recorded a 0.8% year-on-year decline in revenue in Q1 2025, but cut its losses by 73%.

Beyond Meat’s fortunes worsened in Q1 after two quarters of revenue hikes, with sales dipping by 9% in the first three months of this year, with its founder and CEO Ethan Brown suggesting misinformation played a big part. Like Oatly, he added that the “truth is starting to come out” now, and that the meat alternative maker has “made it through that really intense pressure cooker”.

Despite its disappointing sales, it did receive $100M in debt financing from Unprocessed Foods, a wholly owned subsidiary of Ahimsa Foundation, proving that investors still have an appetite for plant-based burgers. “The overall macro environment is challenging for alt-protein, but we are confident of the leadership and the outlook,” Ahimsa Foundation president Shaleen Shah told Bloomberg News.

The volatility of the market was highlighted by Meati’s $4M sale this month. Once valued at $650M, its $100M Series C round was the largest alternative protein investment of 2024, but a technical default led its lender to unexpectedly sweep two-thirds of its cash reserves, leading to the sale at the paltry valuation.

One of the issues in alternative protein is that there aren’t enough exits for startups, though there has been a rapid wave of M&A in the sector of late, from Danone and Chobani’s acquistions of Kate Farms and Daily Harvest, respectively, this month, to Ahimsa Foundation’s takeover of Wicked Kitchen, Simulate and Blackbird Foods in the last year. But exits like Meati’s don’t fill venture capitalists with confidence.

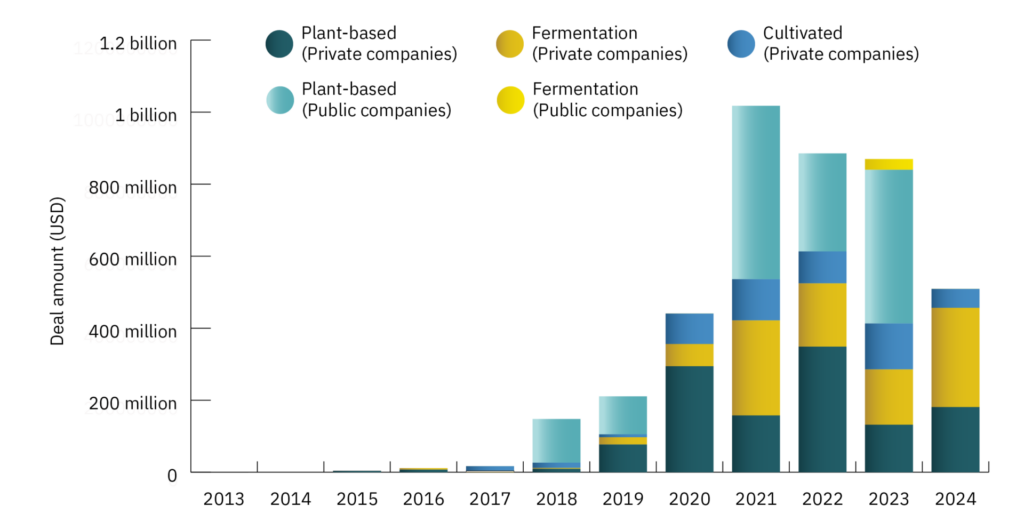

It’s worth noting that despite the VC decline, public sector investment was still strong in 2024, reaching $510M, in line with the year before.

“Going forward, the companies demonstrating clear competitive advantages, unique value propositions, and strong business models will have the best chance of securing funding,” Gertner tells Green Queen.

“However, venture capital is only one piece of the investment puzzle,” he adds, outlining the importance of additional avenues for companies pursuing investment, like equipment leasing, strategic partnerships, sovereign wealth funds, blended finance, and government programmes.

“Alternative protein companies and founders should continue exploring these creative and multipronged funding strategies to support growth,” he says.