Why These Asia-Pacific Countries Are the Ideal Global Hubs for Biomanufacturing

Thailand, Vietnam and Australia have abundant raw materials and forward-thinking public policies, making them potential global hubs for fermentation-derived food production.

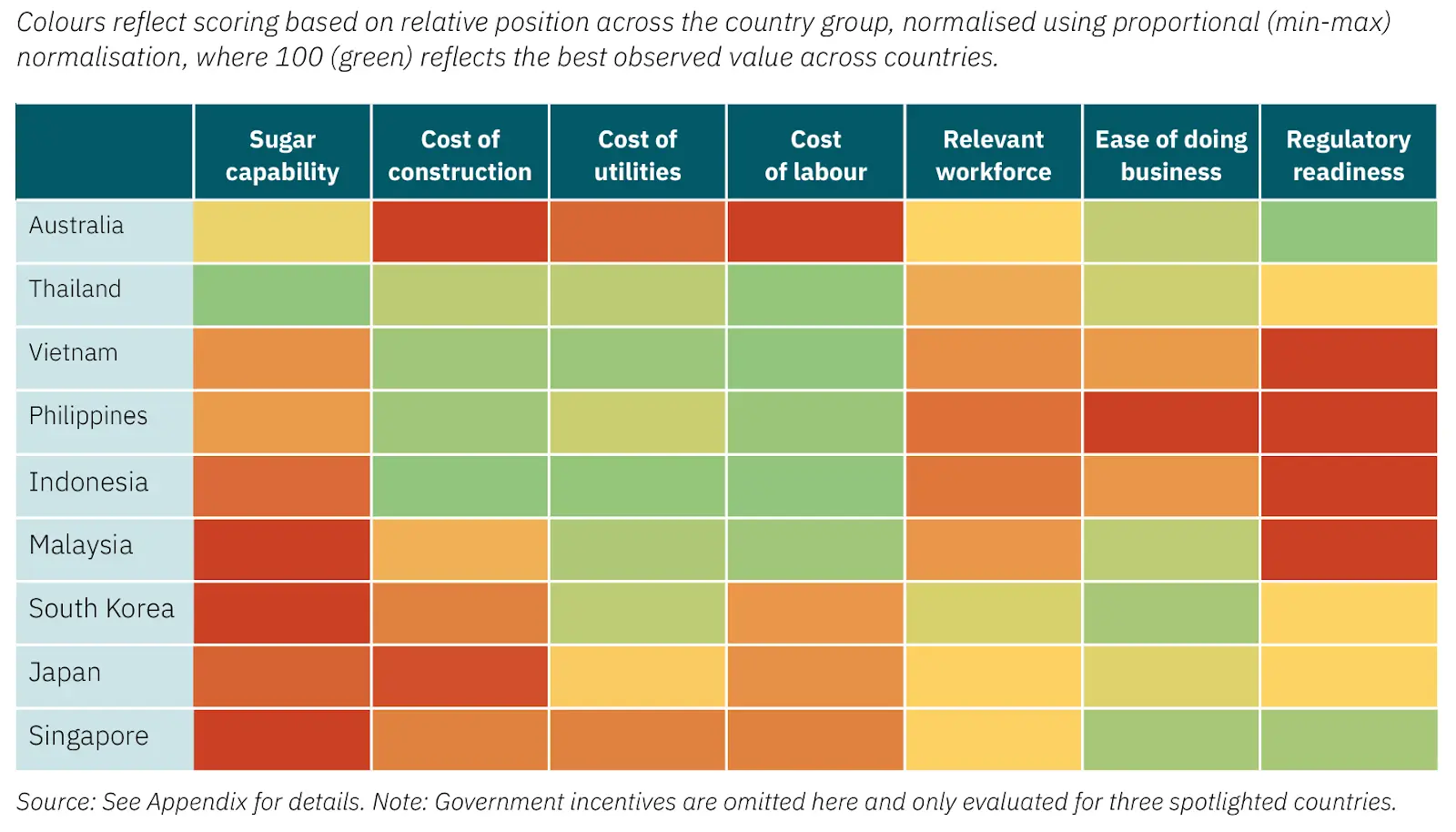

Asia-Pacific could be a global biomanufacturing centre for future-friendly proteins, fats and other ingredients, and three countries stand out in particular, new analysis shows.

Conducted by Hawkwood Biotech on behalf of the Good Food Institute (GFI) APAC, the report suggests that alternative protein stakeholders should keep an eye on Thailand, Vietnam and Australia when choosing where to set up biomanufacturing sites.

The researchers assessed nine APAC countries across key site selection drivers for biomass and precision fermentation, including feedstock and labour costs, ease of doing business, and regulatory readiness.

They chose the three aforementioned nations for deeper evaluation thanks to their performance on these indicators, and further analysed the role of government incentives (which can significantly influence site selection). This was identified as the most critical driver, alongside feedstock costs.

Interestingly, interviews with executives of Fortune 500 bioscience firms and industrial biotech companies reveal that tax incentives are by far the most important factor for site selection among industry leaders (cited by 83%).

This differs from the most high-impact incentives governments could offer, so there may be more impactful incentives that fermentation companies could request to best accelerate domestic biomanufacturing progress, said GFI APAC.

The report highlighted why Australia, Thailand and Vietnam are the most suitable countries for biomanufacturing in the region, and what they need to do to bolster their attractiveness to companies across the world.

Thailand: leading incentives, but lack of regulatory clarity

Thailand is the world’s second-largest exporter of raw sugar, offering strong feedstock availability for industrial-scale fermentation, not to mention it boasts one of the most competitive cost environments for labour, utilities and capital expenditure.

In addition, the Southeast Asian country stands out for its generous government incentives. For example, it offers corporate income tax exemptions for up to eight years, plus a reduction of 50% for an extra five years for eligible companies. Machinery and R&D inputs face full or partial import duty exemptions, and employee training programmes get enhanced deductions (by up to 200%).

Several mechanisms are designed to attract investment in high-priority sectors, and two bodies support Thailand’s bioeconomy strategy by providing R&D infrastructure and boosting microbial strain development.

That said, the country’s potential as a biomanufacturing location is diluted by uncertainty in the regulatory environment. It has a novel food framework in place, though it lacks clear safety assessment guidelines, and has yet to approve a fermentation-derived food for sale.

“This deters investors seeking predictable timelines and streamlined product approval processes. It also highlights the absence of a vertically integrated strategy that combines regulatory enablement with fiscal support to attract commercial-scale fermentation projects,” the report states.

GFI APAC recommends that the country create a coordinated national biomanufacturing strategy that integrates incentives, regulation, and enabling infrastructure, as well as issue guidance on how such projects align with incentive eligibility. Further, Thailand must develop clear, fast-track regulatory pathways for fermentation-derived food ingredients.

Vietnam: an emerging location with supportive policies

Like its neighbour, Vietnam is home to one of the cheapest cost environments for utilities, labour and capex. And while the company’s infrastructure and policies are conducive to a strong biomanufacturing sector, many aspects are still immature.

For instance, Vietnam has moderate technical education levels but limited research capacity, indicating a supportive environment for manufacturing with less alignment with innovation-led scale-up. And though it produces sugar domestically, its limited export volumes suggest a lack of surplus and, subsequently, limited supply at scale.

Moreover, the country lacks a novel food framework. However, the Vietnamese government has been working to improve its bioeconomy, with a recent resolution identifying biotech as a priority for socio-economic growth.

“Strategies outlined by the resolution to achieve these goals include infrastructure investment, human capital development, regulatory framework development, and attracting foreign investment and technology transfer,” the report states.

Plus, Vietnam has made a significant investment in a large-scale biomanufacturing facility, and provides incentives like a four-year tax holiday (followed by a 50% reduction for nine more years) and import duty exemptions.

GFI notes that Vietnam should operationalise the biomanufacturing resolution via funded programmes and specific agency mandates. It should also clarify incentive eligibility criteria, timelines, and

applications for biomanufacturing sites, and publish regulatory procedures and timelines for novel food approvals.

Australia: Strong on policy, weak on incentives

While Australia is one of the world’s leading sugar exporters, too, its labour, utilities and construction costs are far removed from the inexpensive environment in Thailand and Vietnam. Pair that with a lack of incentives and fragmented government support, and the country risks losing out to lower-cost markets.

Interviews with industry and policy experts indicate a dearth of biomanufacturing-specific funding. And existing programmes favour projects with fast timelines and returns, often directing support to legacy industries like mining, energy, and conventional agriculture.

Within biomanufacturing, most attention remains on biofuels, not food ingredients. This reflects not just a “policy preference for incumbent industries”, but also the fact that the value proposition of food biomanufacturing is yet to be fully articulated to lawmakers.

There are some signs of progress at the state level, notably in Queensland, which has been supporting biomanufacturing projects since the mid-2000s. That being said, these efforts fall short in attracting large-scale investment in the absence of a national strategy and biomanufacturing-specific incentives.

One area where Australia’s bioeconomy shines is regulatory readiness. Its food safety framework is among the most advanced globally, giving novel food producers a clear path to securing approval. It has already cleared Impossible Foods’s precision-fermented heme ingredient, allowing the startup to sell its vegan burgers in the country.

To boost its bioeconomy potential, Australia needs to better communicate the value proposition needed to prioritise these ingredients, introduce targeted capex support for fermentation infrastructure, and further streamline approvals to match other regulatory clarity in other domains, like the safety assessment and labelling of ingredients made with gene technology.

The country should set up a federal body to align biomanufacturing policy, funding, and regulatory pathways across agencies, and ensure state-level efforts are reinforced by the national government.