These Are the World’s Best Plant-Based Dairy Products, According to 2,000+ Non-Vegans

Plant-based barista milks and coffee creamers have closed the flavour gap with dairy, though the average non-dairy product still has some way to go. Price and protein wins, meanwhile, will be key to the category’s future.

In the US, 83% of plant-based milk drinkers switched back to dairy in 2025, according to market research agency SPINS. Nothing is a bigger driver of this shift than how these products taste.

Last year, a global survey revealed that 57% of consumers are resistant to non-dairy milk because they’re unsatisfied with its taste or texture. And among the 38% of people who don’t buy these products, 58% showcase the potential to switch if certain needs are met – better flavour being top of the list.

It outlines the need for continued innovation in the dairy-free category, which remains the most well-established segment in the plant-based food market. This momentum is therefore being spearheaded by companies that lead the sensory charts.

The best-tasting products raise the bar for the rest of the sector, and open the door for many consumers who otherwise remain sceptical of dairy alternatives.

To find out which innovations are closest to their cow-based counterparts, non-profit Food System Innovations’s sensory insights initiative, Nectar, conducted an extensive blind taste test of plant-based dairy products between September and November 2025.

Nectar evaluated 98 dairy-free products across 10 categories, pitting them against their dairy equivalents in applications that mirror real-world consumption. Each product was tasted by at least 100 consumers, with a total of 2,183 non-vegans participating in restaurants in New York City and San Francisco.

The findings are highlighted in Nectar’s third Taste of the Industry report, and its first dedicated to plant-based dairy. A total of 27 products were rated as good or better than their dairy counterparts by at least 50% of consumers, and the brands behind them are being recognised with a Tasty Award at a ceremony in San Francisco today.

Coffee creamers the most promising dairy-free category

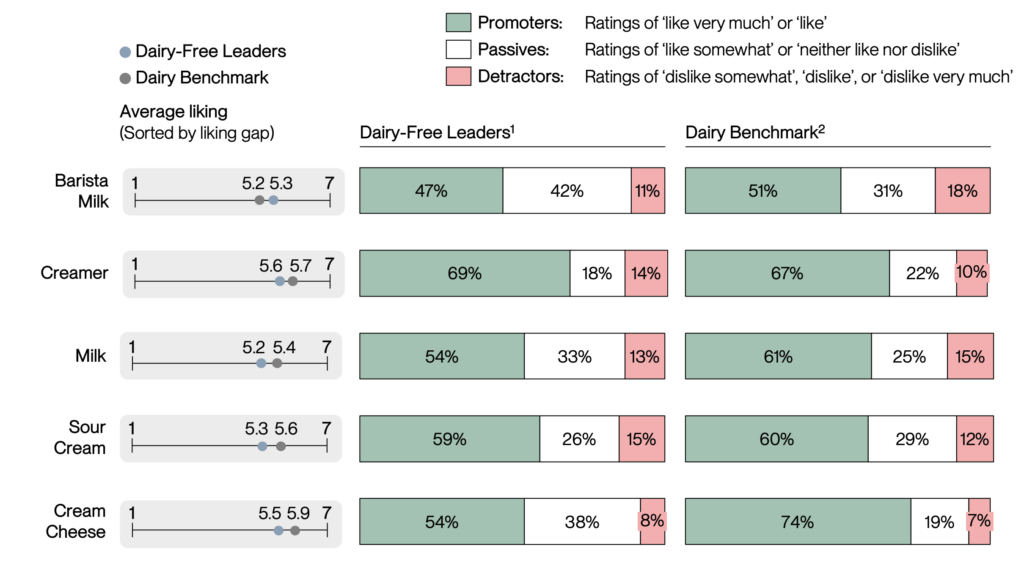

The taste test reveals that some non-dairy products (like barista milks and coffee creamers) are far ahead on the taste parity pathway than others (such as mozzarella and yoghurt).

For instance, 69% of Americans ‘like’ or ‘like very much’ the leading dairy-free creamer products, two percentage points higher than those who say the same for the benchmark dairy product, Chobani’s sweet cream creamer.

Oatly, Planet Oat, Silk, Sown, and Violife all passed the 50% threshold for the Tasty Award, as did Nestlé’s Coffee Mate (which contains less than 2% dairy derivatives and was excluded from the category averages in the report).

In fact, Oatly’s sweet and creamy creamer came within 0.1 points of liking with Chobani’s dairy version. This indicates that it has a 10-50% likelihood of outperforming the dairy benchmark in future taste tests.

“Creamers are heavily engineered products on both sides. Dairy creamers are often sweetened, flavoured, and stabilised, not simply cream,” says Nectar director Caroline Cotto.

“That levels the playing field considerably: oat-based creamers, in particular, excel at delivering the sweetness and smooth mouthfeel consumers want in coffee, and they’re competing against a formulated product rather than pure dairy richness,” she explains.

Cotto believes creamers are the most likely segment to overtake dairy on flavour preferences this year. “Dairy-free creamers as a category matched or exceeded dairy on purchase intent (5.6 vs. 5.5), which tells you the consumer experience is already there for the best products,” she says.

Barista milks close in on taste parity with dairy

Barista milks, emerged as the other category going toe-to-toe with dairy, with 47% of participants liking the leading brands, compared to 51% who said the same for cow’s milk. These products benefit from both “a favourable application context and years of targeted R&D”, according to Cotto.

“Testing in a hot latte is inherently more forgiving than drinking milk straight – coffee shares the flavour stage, and oat milk’s natural sweetness and creaminess complement it well. The category had the smallest liking gap of any we tested, just 0.6 points behind dairy,” she says.

The leader here is Califia Farms’s barista oat milk, which was the only product in the entire study to achieve statistically significant taste parity with dairy: 35% of participants preferred this, and 35% preferred whole milk from Horizon.

“Our qualitative data pointed to its richness and creaminess as key strengths, with notably fewer off-flavours or bitterness complaints than its competitors. The check-all-that-apply data points to its silkiness and smoothness as key differentiators. It’s proof that taste parity is achievable right now,” says Cotto.

Ripple’s barista pea milk and Dream’s barista oat were both found to be within 0.1 points of liking with whole milk. Other barista milks that qualified for a Tasty Award include the oat milks from Planet Oat and Minor Figures, and Milkadamia’s macadamia milk.

“A broader pattern seems to be emerging that coffee-application categories, where the flavour experience is shared with the coffee beans themselves, are systematically outperforming dairy-free products tested in isolation,” says Cotto.

Indeed, when it came to non-barista milk alternatives, the likeability gap was slightly wider among the leading products, which were enjoyed by 54% of taste-testers, versus 61% who liked Horizon’s 2% milk. Here, Blue Diamond’s Almond Breeze, Maïzly’s corn milk, and Silk are the Tasty Award winners.

Closing the gap between the average and leading dairy alternatives

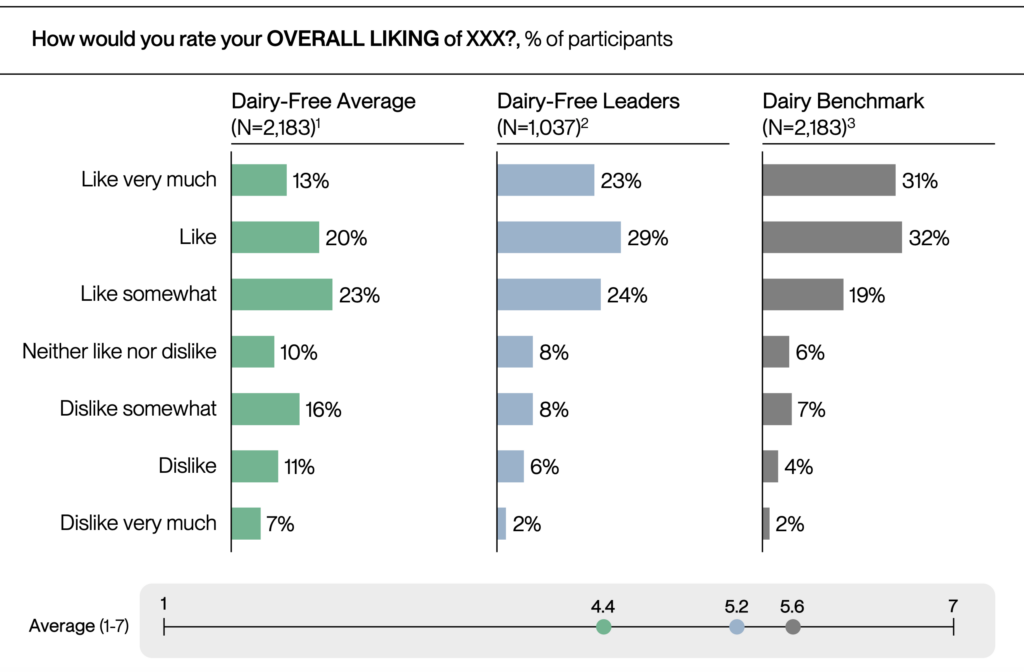

The survey suggested that dairy still enjoys higher overall likeability (82%) than the average plant-based alternative (56%), though the gap with the leading non-dairy products (liked by 76%) is much smaller.

In fact, the difference in purchase intent between the dairy-free average and the dairy benchmark is 1.2 points, with eight out of 10 categories showcasing a gap of at least one point (barista milk and Cheddar cheese were the outliers).

Further, the research highlights the chasm between the category average and the leading products, which outscored the former by 0.8 points in overall liking. Only 17% of Americans said they disliked the dairy-free leaders, half as many as those who felt this way for the average product (34%).

“The gap comes down primarily to flavour, specifically off-flavours and off-aftertastes. In our qualitative data, flavour was cited as a dislike two to four times more often than texture or appearance,” says Cotto.

“Leaders have largely solved this: no beany notes, no chemical aftertaste, no unexpected bitterness. They’ve also cracked richness: the fat-driven mouthfeel and depth that consumers associate with satisfaction.

“The result is a product that doesn’t ask omnivore consumers to overlook anything. The average dairy-free product earned ‘like’ or ‘like very much’ from 33% of participants; the average leader hit 51%.”

By far, the category that requires the most work to catch up with its animal-based equivalent is mozzarella, which only 25% of respondents are willing to purchase (compared to 67% who’d buy conventional mozzarella).

“The dairy-free average scored 4.0 versus 6.1 for the dairy benchmark – a 2.1 point gap – and even the category leader sits 1.4 points behind dairy, the largest leader-to-benchmark gap we measured. It was the only category with zero Tasty Award winners,” says Cotto.

“For mozzarella, the biggest challenges are texture and function: plant-based mozzarellas must melt, stretch, and brown, while also delivering a rich milky flavour. Dairy casein is uniquely suited to this. Many current plant-based formulations rely on starches and non-dairy fats that consistently fall short,” she notes. “The upside is that the white space for a true category leader is enormous.”

Aside from taste, price a ‘gatekeeper’ for mass adoption

Despite the spotlight on taste, several other factors will contribute to how well plant-based dairy does in the future. Conceptually, 55% of consumers think non-dairy products are better for their health than those derived from cows (which only 29% believe are healthier). In fact, 48% ‘strongly agree’ that health factors into their purchasing decisions in the dairy-free category.

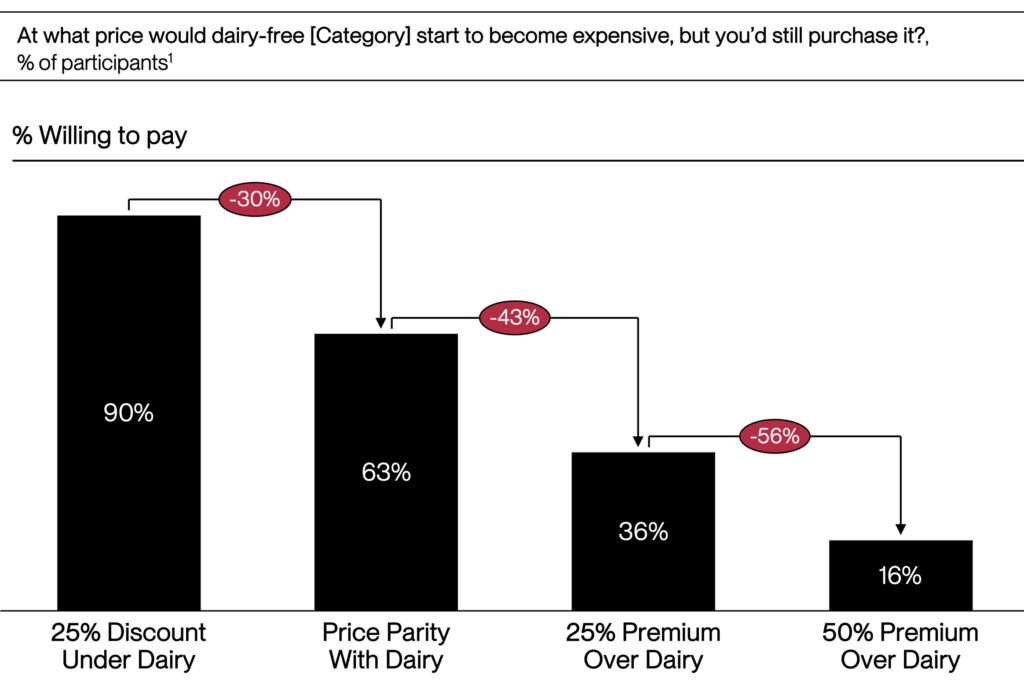

This was only trumped by taste (60%) and price (62%), which can drive long-term mass appeal. Only 13% of Americans find non-dairy products to be better for their wallets. If they were 25% cheaper than dairy, 90% would be willing to buy them, but this drops to 63% if they’re priced the same, and 36% if they carry a 25% premium.

“The numbers are unforgiving,” says Cotto. “A 25% premium over dairy prices out 43% of consumers; at 50% premium, only 16% remain willing to pay. Consumers also think in absolute dollars, so the gap feels largest in categories where dairy itself is expensive.”

The solution requires parallel progress on two fronts. “Ingredient cost reduction through scale and innovation (precision fermentation and novel fats are key), and consumer-facing tactics like smaller pack sizes that shrink the absolute dollar gap,” she explains.

“Ultimately, taste improvement and market share growth are a virtuous cycle. Better taste drives sales and scale. Scale drives cost down, which drives adoption, which funds further R&D.”

Taste and price are the “gatekeepers” for mass adoption. “Price, in general, is becoming an increasingly important focus for consumers as groceries become more expensive due to larger macroeconomic factors like tariffs and international conflicts affecting fuel and import costs,” says Cotto.

Protein increases purchase intent but lowers product performance

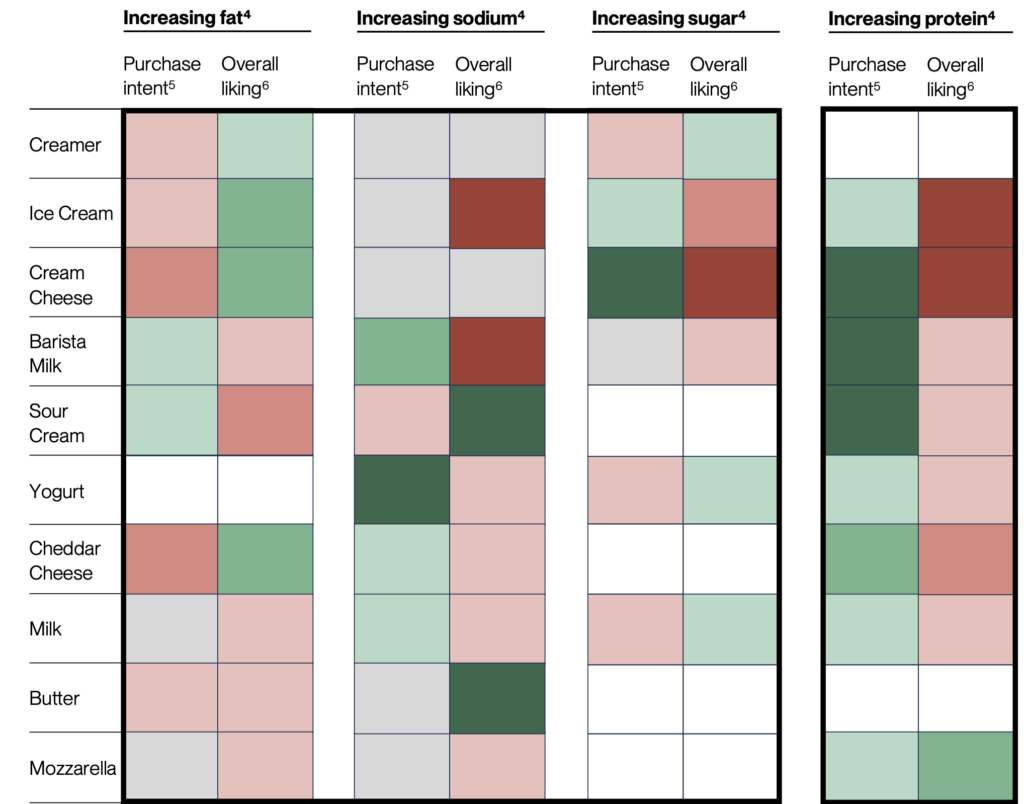

Another aspect to look out for is protein, a macronutrient that is top of mind for a majority of Americans. More and more brands are launching protein-boosted plant-based milks, including Silk, Califia Farms, and Elmhurst 1925. This is a shrewd move, since protein is the only macronutrient that had a significant correlation with purchase intent and liking in Nectar’s survey.

The presence of protein had the strongest positive impact on barista milks, cream cheeses, and sour creams. However, there is a caveat: increasing protein content can negatively affect product performance, as is most evident in cream cheese and ice cream.

It calls for a fine balancing act: brands looking to amp up protein levels must factor in potential detriments to the product’s flavour. This dichotomy exists with ingredients, too. Cashews and almonds increase the purchase intent but end up damaging the likability, while sunflower oil and peas decrease consumers’ willingness to buy plant-based dairy products, but improve their chances of liking them.

Nectar revealed that Americans are more likely to notice proteins than oils, with ingredients in the former category reported by at least 20% of consumers as having an impact on their purchase intent, versus 16% for oils on average.

For most categories, amplifying the richness seems to be the top R&D opportunity. But this isn’t as simple as just adding more fat or sugar. “Macronutrient levels showed mostly weak or neutral correlations with liking across categories, or said otherwise, adding fat or sugar on a per-calorie basis didn’t reliably improve scores,” says Cotto.

“Richness in sensory terms is about mouthfeel, flavour depth, and the absence of thin or watery notes – properties dairy achieves through its specific fat structures and proteins working together,” she explains. “The most promising R&D pathways involve precision fermentation, better emulsification, and novel ingredient combinations, not simply more commodity fat/sugar.”

She adds that people’s concerns around nutrition were “more sophisticated than expected”. “Protein had a clear positive effect on purchase intent; fat and sugar largely didn’t register. Ingredients broadly had minimal impact once labels were revealed,” Cotto notes.

“I don’t see the risk as consumer backlash, but rather that just adding fat and sugar probably won’t even work to mimic the richness that traditional dairy consumers are demanding.”

Why plant-based dairy products are ahead of meat alternatives

Reflecting on how brands can market plant-based dairy better, the Nectar director reckons they should lead with protein content and genuine nutritional advantages. “Our data suggests clean labels highlighting protein matters more than ‘free from’ messaging, though this is an area we’re continuing to research,” she says.

Sustainability messaging, though, doesn’t move this group. Emotionally, brands need to evoke joy, comfort, and indulgence, which currently influence more dairy purchases, and avoid triggering suspicion or disappointment.

“Based on the abundance of mis- and disinformation surrounding plant-based products, consumers note that they can feel deceived by dairy-free products or suspicious of product claims and benefits,” says Cotto.

Enhancing the sensory profiles of non-dairy products can drive financial returns, too, with improved taste strongly correlated to higher market penetration. Milk is a prime example: it’s the best-tasting non-dairy category, and holds a market share 15 times larger than cheese, the worst-tasting segment.

Nectar’s previous taste tests have focused on meat alternatives, many of which still suffer on the taste scale. Cotto points out that the 27 dairy-free products that meet the threshold for this year’s Tasty Awards represent a 72% increase from the meat-free products that won in 2025, when adjusted for the number of brands tested.

“I think there are a few reasons. First, the sensory target is more approachable: dairy’s core attributes, such as creaminess and smoothness, are more readily approximated by plant-based ingredients than the fibrous, juicy qualities of whole-muscle meat,” she says.

“Second, the category has simply had more time: oat and soy milks have been iterating for decades, while plant-based meat at scale is a much younger category. Third, there’s a real consumer driver for dairy-free products that does not exist with meat alternatives: lactose intolerance. An estimated 68% of the global population experiences some degree of lactose malabsorption, making dairy inaccessible to billions.

“Lastly, consumer expectations also play a role. Many omnivores have years of experience with non-dairy milks in their coffee and have recalibrated accordingly. Or, they’ve even created novel use cases for these products, like in smoothies, where dairy milk is less common.

“The expectation gap for dairy alternatives is narrower than for plant-based meat, where consumers are still comparing products to the full sensory experience of a burger or sausage.”