Billions of Dollars Marketed As ‘Green’ Are Quietly Fuelling Deforestation

From Brazil’s cattle pastures to Indonesia’s palm oil plantations, European “green” funds that claim to combat climate change are financing companies tied to deforestation and rising emissions, shows a new investigation by Green Queen Media.

Despite pledges to protect biodiversity, the world’s largest asset managers are still pouring billions through “green” funds into food companies driving deforestation, all while scientists warn that halting forest loss this decade is crucial to controlling global warming.

In the second quarter of 2025, banks and asset managers held almost $9B in “green” investments across 10 major food and agribusiness multinationals exposed to deforestation, according to an investigation by Green Queen Media, using data sourced from the London Stock Exchange Data & Analytics and Global Canopy.

These funds claim to follow strict environmental, social, and governance (ESG) criteria, with some marketed as “Climate Paris Aligned” or “Global Sustainable Food and Water”. They are managed by leading financial management institutions, including Amundi, JP Morgan, DWS/Deutsche Bank, and BlackRock.

High deforestation risk in ‘green’ funds

Ten global food and agribusiness companies with high to critical exposure risk to deforestation in their supply chains are sponsored by “green” funds, while some of them have open deforestation controversies in different biomes, including the Amazon Rainforest, where the COP30 was held in November.

Some of them are large multinational food corporations, such as US-based Mondelēz International or Mexican Grupo Bimbo, which, according to the latest Forest IQ assessment, are rated as respectively having “critical” and “very high’ risk exposure to deforestation for soy and palm oil, where “critical” is the worst rating of deforestation exposure.

Mondelēz and Grupo Bimbo in the second quarter of 2025 together received $5.1B in “green” investments*. The funds we identified are those disclosed under the EU’s Sustainable Finance Regulation (SFDR), which came into force in 2021.

Having high to critical exposure means that companies are linked to large volumes of these commodities produced in countries where there is a considerable deforestation risk.

Mondelēz International, which sells its chocolate, chips, and biscuit snacks containing palm oil and soy in more than 150 countries, is the main recipient of “green” funds among the ten companies analysed. The company recently called for a one-year delay of the Regulation on Deforestation-free Products (EUDR), a landmark European law that was supposed to go into effect at the end of 2025 and is aimed at blocking deforestation-linked products from entering the bloc.

Lobby efforts to delay it have been successful, with the EU Parliament voting to extend the deadline to the end of 2026 for large players and mid-2027 for smaller companies. The EUDR has now been delayed for one more year. Moreover, leading soy traders analysed by this investigation, such as Cargill and Bunge Global, have exited the Amazon Soy Moratorium, one of the world’s most important rainforest conservation agreements.

Others, such as the Brazilian meat giants JBS, Marfrig, and Minerva, have faced multiple controversies about their supply chains, with accusations of deforestation and land grabbing.

JBS is the world’s largest meat company, selling a large variety of beef and other animal meat products. Despite its promises to end supply-chain-linked deforestation by 2025, a recent Guardian investigation found that problems remained rampant, and that it was highly unlikely that the company would meet its deforestation-free supply chain commitments.

Green funds hold $5M in investments across JBS, Marfrig, and Minerva*. Data sourced by Trase estimated that in 2023, these companies had a risk of deforestation exposure amounting to 522,000 hectares across multiple Brazilian biomes.

While all the companies have high or even critical exposure to deforestation risks in beef, soy, and palm oil supply chains, most of them have low values of reporting and verification on deforestation or biodiversity protection, according to Forest 500 data.

Together, these companies generate an average of around $10B in annual revenue from their core business activities* (2024 LSEG data) – a scale that highlights just how deeply these powerful market actors shape global food and commodity chains.

More than 50% of the “green” shareholdings in those companies in the second quarter of 2025 came from the top ten asset managers out of 258 we analysed for this investigation.

German DWS Investment ($1.7B) Belgian Capfi Delen ($636M), Finnish Nordea Funds ($443M), Swedish Cliens Asset Management ($415M), Danish SEB Investment Management ($365M), Spanish Caixabank Asset Management ($321M), the UK-branch of BlackRock Investment Management ($288M), Swedish Swedbank Robur Fonder ($267M) and US JP Morgan Asset Management ($260M).

Together, these asset managers have $4.9B of “green” holdings* into food and agribusiness companies with a high risk of exposure to deforestation.

The dark side of transparency: retail investors likely unaware of harmful investments

The EU Commission in 2021 launched the Sustainable Finance Disclosure Regulation (SFDR), asking financial players to disclose the degree of their alignment with the objectives of the Paris Agreement.

The objective of the regulation was to “help investors who want to put their money into companies and projects supporting sustainability objectives to make informed choices”, but it quickly became a labelling framework to identify investments with environmental and social characteristics (so-called ESG investments corresponding to Article 8 of the regulation) or sustainable investments (corresponding to Article 9 of the regulation).

However, it failed to exclude the most polluting industries, as numerous investigations have exposed. Under regulatory revision, today’s growing “green” segment of European finance attracts €7T in global capital, according to the latest Morningstar data, attracting global private capital from even extra-UE asset managers authorised to operate in the European market by the supervisory authorities.

While Article 5 of the Paris Agreement highlights the importance of “positive incentives for activities relating to reducing emissions from deforestation and forest degradation”, the SFDR is currently failing at creating clear exclusions for deforestation risk.

Indeed, studies have shown that forests store almost half of terrestrial carbon. They also contribute to cooling temperatures by releasing water vapour into the atmosphere. However, in recent years, deforestation has been spiking, with tropical deforestation increasing by 80% between 2023 and 2024, according to the World Resources Institute.

Most of global deforestation happens in tropical forests, and the food industry is the main culprit. Beef, soy, and palm oil are responsible for 60% of tropical deforestation around the world. This means that so-called “green” funds offered by global asset managers are holding stocks of companies with a high risk of being exposed in the supply chain of this 60% of tropical deforestation and realising high shares of emissions.

Asset managers that do not address the issue of portfolio companies with a high risk of deforestation exposure cannot plead ignorance. It is not for a lack of data and tools,” says Pei Chi Wong, strategic finance engagement lead at Global Canopy.

These €9B in investments may well come from European customers who are unaware that they are entrusting their savings to portfolios holding companies with a high deforestation risk. A recent report from the Sustainable Finance Observatory shows that while 74% of EU retail investors have sustainability-related objectives, in 57% of advice meetings these preferences were not automatically assessed.

This means that many clients seeking real-world impact may not have received products aligned with their goals. In addition, current regulations require advisors to disclose only the top 15 holdings in a portfolio, making it difficult for clients to understand the full picture of where their money is being invested.

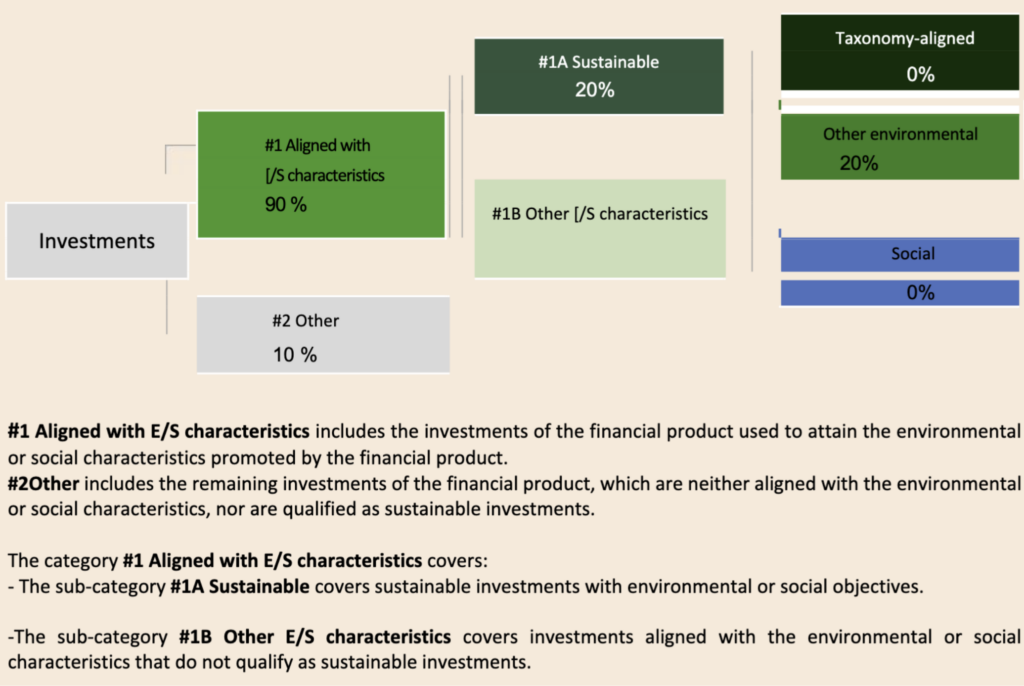

For example, in the second quarter of 2025, the passively managed Amundi S&P 500 Climate Paris Aligned fund invested $27M in Mondelēz International – the company is listed as having critical exposure to deforestation risk linked to soy and palm oil, according to Forest IQ assessment.

In its 500-page prospectus, Amundi states that 90% of the fund’s holdings are aligned with environmental and social characteristics. Yet this information is not disclosed at the entity level, meaning customers cannot know whether Amundi considers Mondelēz to meet those ESG criteria. In its 2024 Principal Adverse Impact report, Amundi also claims to account for activities that harm biodiversity, though no supporting metrics are provided.

In 2025, the Fonditalia Equity Latin America fund, marketed by Fideraum Ireland, invested $513,000 in JBS. Despite claiming that 80% of its holdings promote environmental and social characteristics and that 20% qualify as sustainable investments, the fund’s exclusion criteria do not directly evaluate a company’s deforestation risk.

In the second quarter of 2025, asset managers continued to market funds with ESG or sustainability-linked labels while investing in companies with high deforestation risk. The value of these “green” funds reached $623M*, about 7% of all green investments analysed. Other names used were “Life Climate Aware”, “Equity Climate Transition” or “Ethic Global Trends”.

A European Securities and Markets Authority spokesperson told Green Queen: “SFDR as currently applicable does not have exclusions; it is a disclosure-based framework. It contains very few criteria for financial products that are disclosing under Article 8 or 9 of the SFDR.

“Where financial products make sustainable investments, financial market participants making those financial products available have to show that the financial product’s investments do not cause significant harm (DNSH).”

They added: “For DNSH disclosure purposes, those financial products have to use at least the 18 mandatory indicators in Table 1 of Annex I and the relevant indicators in Tables 2 and 3. There are no indicators related to deforestation in Table 1, but in Table 2, indicator 15 is directly related to deforestation, measuring the share of investments in companies without deforestation policies.”

Are green funds ‘eating the earth’?

As author and journalist Michael Grunwald writes in his latest book, We Are Eating The Earth, deforestation is a major driver of climate change, and it’s mostly caused by agriculture. “Our land problem, it turns out, is mostly an agriculture problem,” writes Grunwald. “Agriculture is by far the leading driver of deforestation.” Grunwald also notes that deforestation is transforming the Amazon basin from a carbon sink into a carbon source.

According to the latest IPCC report, halting deforestation would result in a 25% reduction in global emissions by 2030, and could contribute up to 80% of emissions reduction from land-use activities by 2040-2050.

Asked how so-called green funds can invest in companies with links to deforestation, Josephine Richardson, managing director and head of research at non-profit the Anthropocene Fixed Income Institute (AFII), said: “The average ESG funds have a very low level of business exclusions, and they tend to be focused on unconventional oil and gas production and weapons.

“Asset managers often make use of ESG ratings, and it is difficult to track deforestation in such ratings because often these are large multinational companies with a lot of business activities. Investors should be mindful and understand what products they want and how they want to direct their capital.”

So-called “green” funds are failing to exclude deforestation-linked companies from their portfolios. As a recent report published by AFII shows, ESG funds have, on average, 5.8% exposure to issuers in the deforestation companies; in most cases, they have even higher exposure than a non-ESG equivalent fund.

“Any fund that seeks to credibly claim to be ‘green’ or to tackle climate impacts must address exposure to deforestation, which accounts for 11% of global GHG emissions,” concluded Pei Chi Wong.

The EU’s sustainable finance rules were recently revised by the European Commission with the stated aim of simplifying transparency requirements for asset managers. In the version released on 20 November, entity-level disclosures on funds’ harmful environmental impacts were removed. In practice, this means that companies in SFDR portfolios with a high risk of exposure to deforestation will no longer be individually scrutinised, making it even harder for clients to understand the true nature of their “green” portfolios.

The shift comes as COP30 in Belém, Brazil, launched the Tropical Forest Forever Facility, presented as “a unique opportunity to combine solid fixed-income returns with credible, large-scale nature and climate impact”. COP30 ended with over $6.7B invested in this new climate fund, more than $2B less than the amount of “green” investments in a few companies highly exposed to deforestation. Whether it will attract more Paris Accord-aligned investors in the years to come remains an open question.

Editor’s Note: Green Queen reached out to the asset managers featured in our investigation to ask whether they have specific deforestation-linked exclusions in their investments.

German DWS said in an email statement that it “does not maintain a policy exclusively focused on deforestation. Our actively managed mutual funds based in Europe, which report under Article 8 or 9 of the Disclosure Regulation, exclude companies involved in severe environmental controversies – potentially including deforestation-related issues.“

Swedish SEB Investment Management confirmed its investments in AAK, Mondelēz, Grupo Bimbo, and Archer-Daniels-Midland: “AAK is one of the better performers in the palm oil/agriculture supply chain. Thus, we retain ownership and have regular meetings on these topics together with other investors,” it said, adding that “a company assessed as having high exposure risk to deforestation is not necessarily the same as verified involvement in illegal deforestation. Our approach therefore distinguishes between (i) verified breaches/controversies and (ii) heightened sector/commodity exposure, where our focus is on robust risk management and active ownership.

An SEB spokesperson added: “Our sustainability policy explicitly addresses supply-chain deforestation risk for high-risk commodities. We also encourage full traceability in production processes and supply chains.”

BlackRock declined to comment, and the other firms did not respond.

*All values of “green” investments refer to data we obtained for this investigation from the London Stock Exchange Group data. “Green” funds are those disclosed under the EU Sustainable Finance Disclosure Regulation (2019/2088).