Global Sales of Plant-Based Food Grew by 3% in 2025 Amid Funding Decline: GFI Report

Alternative protein think tank the Good Food Institute has released its State of the Industry reports for 2025, covering plant-based, fermentation-derived and cultivated proteins.

People across the world bought more plant-based meat and dairy products in 2025 than the year before, despite heightened concerns about ultra-processed foods (UPFs) and a continued decline in VC interest, according to the 2026 State of the Industry report series by the Good Food Institute (GFI).

The alternative protein think tank’s annual reports take a deep dive into the commercial, consumer and policy landscape surrounding plant-based, fermentation-derived and cultivated proteins. The 2026 edition spotlights the impact of UPFs, the booming demand for protein, and governments’ dichotomous policies, and how they’ve shaped the food tech market.

It was a year where sales of plant-based food increased in many categories, even if many startups failed to raise money and reached the end of the road, and several novel food products earned regulatory approval, despite attempts (many successful) to restrict the labelling or sale of innovations like cultivated meat.

The overall reading, though, skews positive, signalling a period in which many expect the alternative protein sector to rebound after several years of correction.

Global plant-based sales increased, with Europe taking the lead

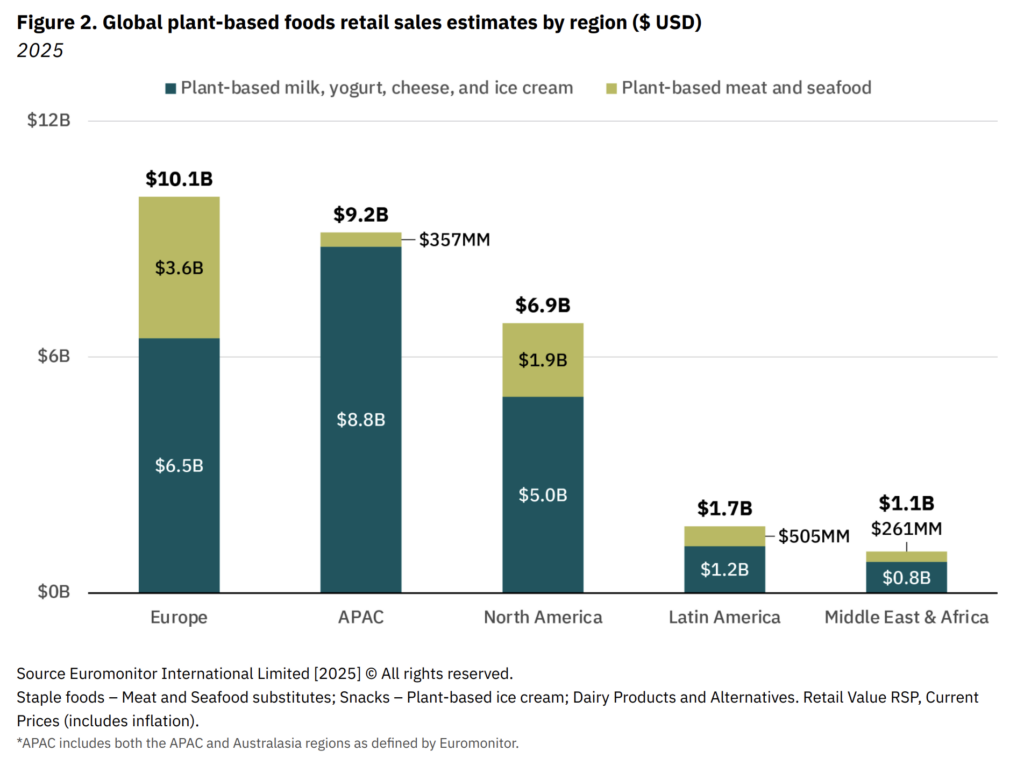

Retail sales for plant-based meat, seafood, and dairy reached $28.9B worldwide in 2025, according to analysis by Euromonitor – that’s a 3% increase from the year before (including inflation).

Non-dairy products continued to lead this market, totalling $22.7B (accounting for 78.5% of all plant-based sales). This represents a 2% increase from 2024, while volume sales flatlined. In terms of specific segments, milk alternatives topped the charts with $18.2B in sales.

But plant-based meat had an even more impressive 2025, with retail sales estimated at $6.6B, up by 8% year-on-year and 4% when adjusted for inflation. Volume purchases grew by 3% as well, suggesting they drove overall sales.

The success of the meat analogue category was driven largely by an uptick in Europe, which remains the biggest market for plant-based food globally – total sales for meat and dairy alternatives reached $10.1B in the continent. This is followed by Asia-Pacific ($9.2B) and North America ($6.9B).

US sales for plant-based meat and milk declined, despite bright spots

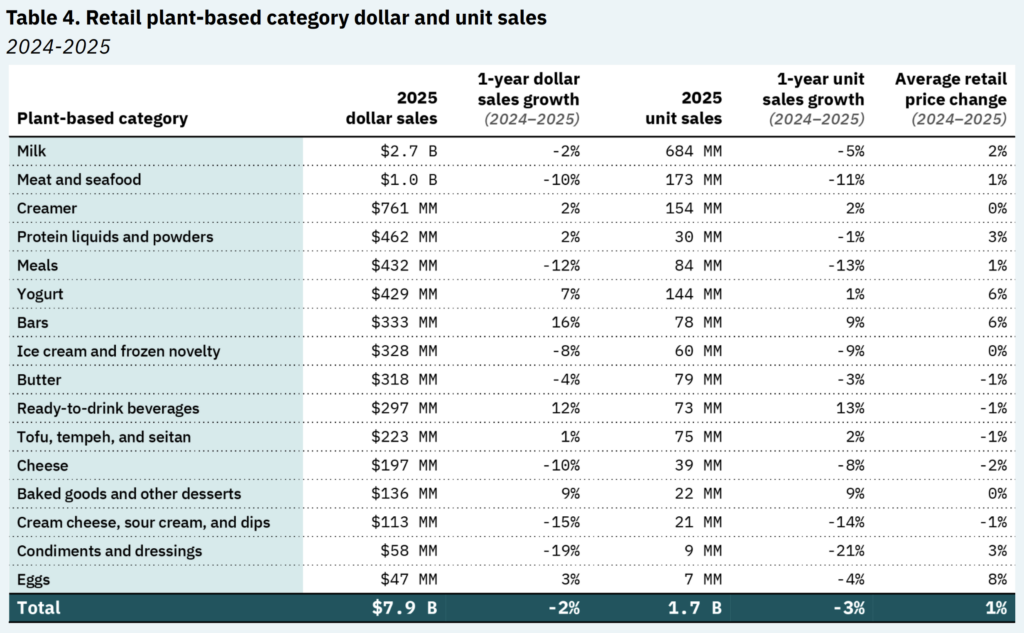

Headwinds for the plant-based sector in the US were reflected in the market data for 2025, with overall sales recorded at $7.9B, a 2% drop from the previous year, according to SPINS.

Plant-based meat and seafood continued to struggle, with dollar sales down by 10% (reaching $1B) and unit sales by 11% last year. Non-dairy milk, meanwhile, was the largest category, with $2.5B in dollar sales – though this represented a decline of 2%.

That said, several formats within these categories experienced growth in 2025, including soy and coconut milk (up by 4% and 27%, respectively), and chunks, shreds and strips (an 8% hike in unit sales).

Other segments that enjoyed a successful year in terms of retail sales include bars (16%), ready-to-drink beverages (12%), baked goods (9%), yoghurts (7%), eggs (3%), creamers and protein powders (2% each). Purchases of tofu, tempeh and seitan witnessed a small 1% bump.

In the foodservice sector, total broadline distributor sales of plant-based proteins (including meat alternatives, tofu, tempeh and veggie burgers) reached $291M in 2025, a 7% decline in dollar sales. But several plant-based meat formats experienced an uptick – as did milk alternatives, which recorded $288M in sales (up by 14%), and creamers, which saw a 4% rise to $189M.

Some plant-based products are getting cheaper, but they’re reaching fewer consumers

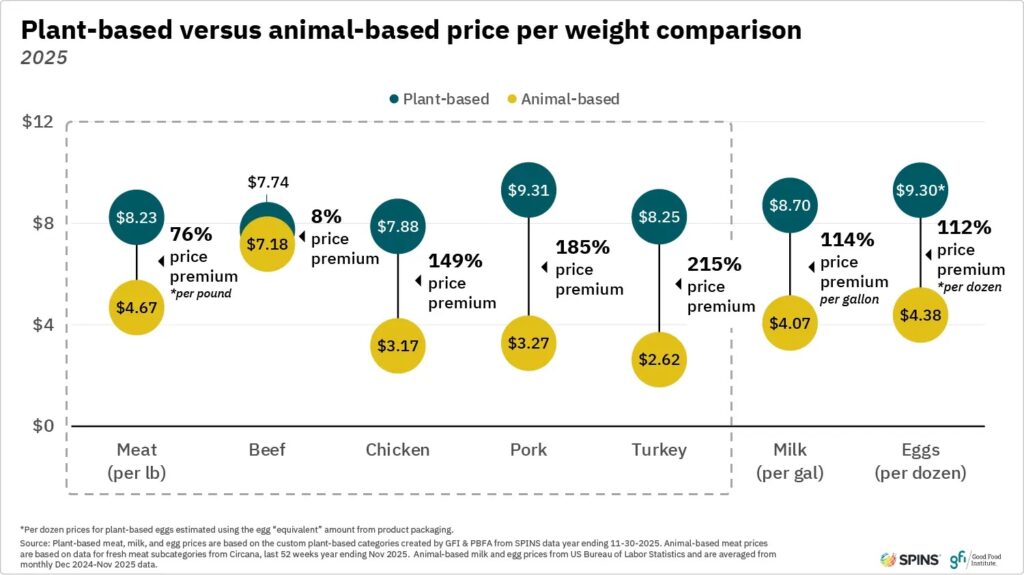

Inflation had an outsized impact on the food supply in 2025. Still, the price of plant-based meat in the US rose only 1%; in fact, products like butter, ready-to-drink beverages, cheese, tofu and tempeh, and sour cream and dips became more affordable.

However, plant-based milk was 2% more expensive in 2025, reversing its decline from the previous year. Eggs experienced the largest hikes in price (8%), followed by yoghurts and bars (6% each).

In a positive sign for the industry, the gap between meat and vegan alternatives narrowed – the latter carried a 76% price premium in 2025, down from 82% in 2024. Unsurprisingly, plant-based beef is closing in on its conventional counterpart (with just an 8% premium), reflective of beef’s record-breaking prices in the US last year.

The prices for chicken and pork maintained their gaps in 2025, but plant-based milk is now 114% more expensive than cow’s milk, and vegan eggs 112% costlier chicken-derived versions.

Penetration of these products also contracted last year. Overall, 60% of US households purchased a plant-based SKU, and 78% came back for more. However, this figure declined for both milk and meat alternatives, whose penetration stood at 38% and 11%, respectively. Repeat purchases remained steady at 75% and 62%.

Overall, vegan meat and seafood products accounted for just 1% of total retail sales of meat in the US, much lower than the 13% milk market share occupied by non-dairy alternatives.

VC funding reaches seven-year low, as public investment soars

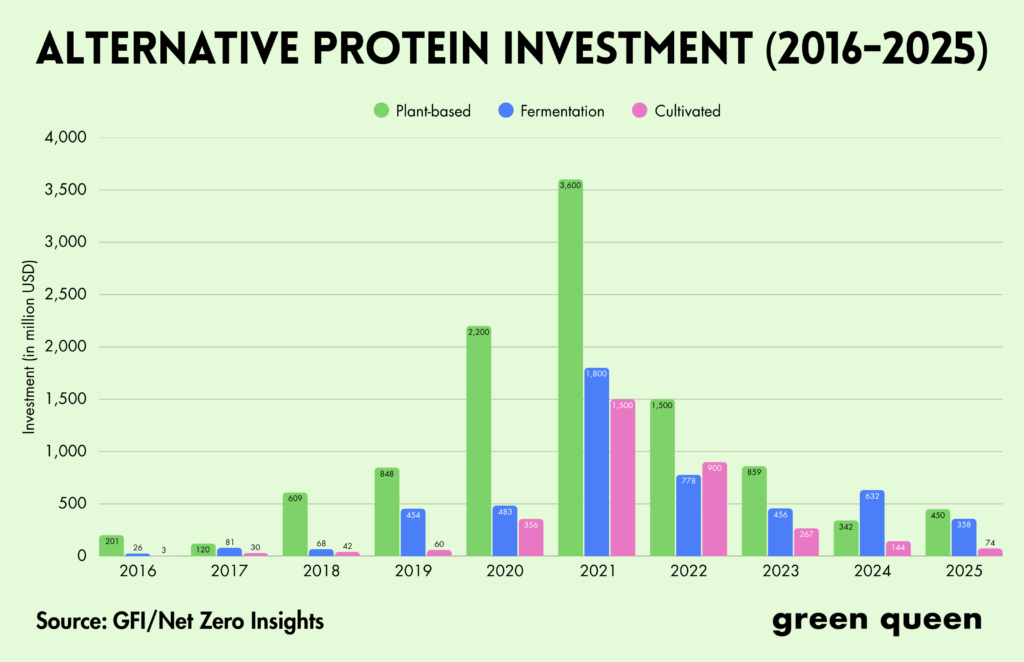

As reported by Green Queen in February, GFI’s analysis of Net Zero Insights data shows that funding for the alternative protein sector fell by 20% in 2025, attracting just $881M. It was the first time this figure fell below the $1B mark since 2018.

Investment in fermentation companies totalled $357M, a 43.5% dip from the highs of 2024. Cultivated meat fared far worse at a total of $74M (nearly half of its funding sums from the previous year).

Plant-based was the only segment to surpass its 2024 total, reaching $450M (a 31.5% increase), but this was helped by Beyond Meat’s $100M debt financing round. Without it, funding for the plant-based category would have increased by only 2%.

That said, governments continued to pour in major sums into the alternative protein ecosystem. In 2021, collective public funding for the sector totalled $700M – this grew to $2.5B in 2025, a more than fourfold increase in as many years, driven by China and the EU. Likewise, the number of countries working to advance this industry has doubled from 16 to 33.

Consolidation remains prominent in the alternative protein sector

Analysis by Green Queen has found that, since September 2024, more than 70 alternative protein businesses have merged, been acquired or bought out, fallen into insolvency, or ceased operations.

GFI’s 2026 State of the Industry reports attribute this wave of consolidation to the sector’s funding troubles. Last year, 19 plant-based companies were acquired, and several others paused or ceased operations after struggling to secure follow-on financing.

This was true for the cultivated meat space as well. Unsuccessful fundraising efforts and ongoing financial troubles led to the demise of leading startups like Meatable and Believer Meats. Others took the M&A route to leverage external technologies and boost innovation: Nexture Bio took over Matrix FT, Gourmey merged with Vital Meat to form Parima, and Fork & Good acquired Orbillion Bio.

The fermentation category did not witness the same pace of consolidation, but a few high-profile closures and restructurings “tested assumptions around timelines, scale-up pathways, and downside risks”. Bolder Foods, Arkeon, NovoNutrients and Planetarians all called it quits. Libre Foods was acquired by Planetary, and Meati Foods was rescued from the brink in a $4M buyout.

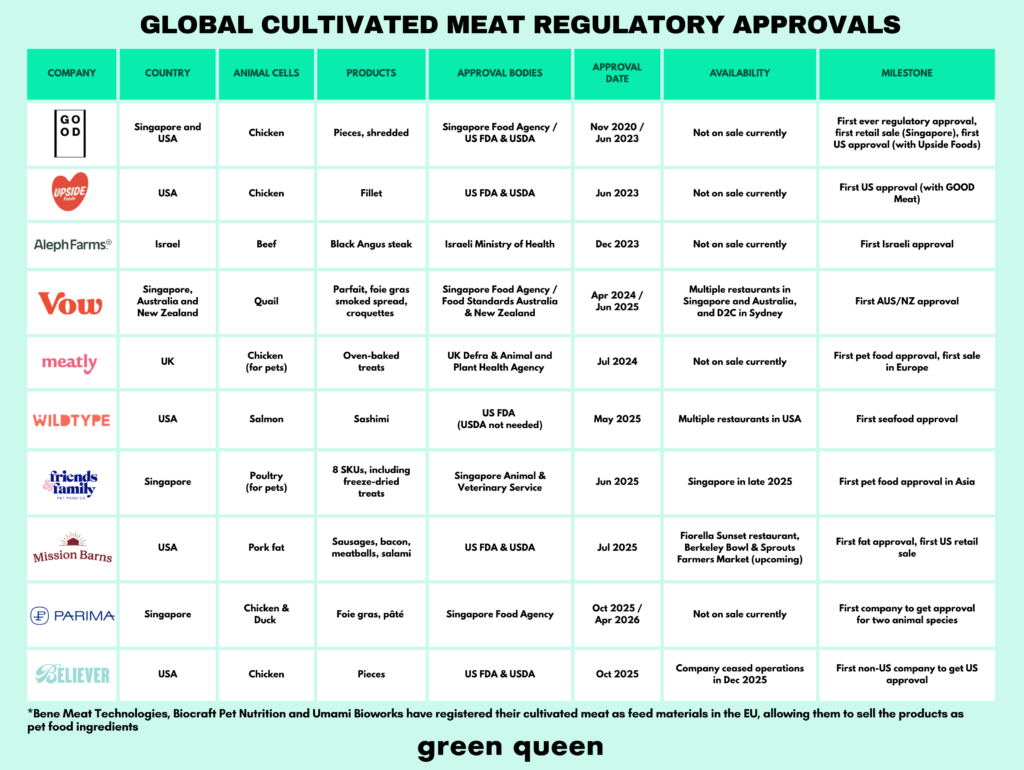

Regulatory milestones offset by legislative challenges

2025 was a milestone year for cultivated meat regulation, with six companies receiving approval to sell their products for human or pet food: Vow (Australia), Wildtype, Mission Barns, Believer Meats (all US), Friends & Family Pet Food Company and Parima (both Singapore).

Many fermentation-derived ingredients also cleared regulatory hurdles. In the US, 10 precision- and biomass-fermented products obtained a ‘no questions’ letter from the Food and Drug Administration, while several more self-determined their ingredients as Generally Recognized as Safe (GRAS).

However, these regulatory wins coincided with many legislative battles faced by the alternative protein sector. For one, the self-affirmed GRAS pathway is set to be eliminated under the directive of health secretary Robert F Kennedy Jr, which would increase the time and money it takes for companies to earn approval.

Meanwhile, following the lead of Florida and Alabama in 2024, five other US states – Mississippi, Montana, Indiana, Nebraska, and Texas – banned the sale of cultivated meat last year (South Dakota joined them last month).

And in the EU, policymakers agreed last month to prohibit companies from using 31 meat-related terms on the packaging labels of plant-based and cultivated protein products, after months of intense debate in 2025.

“Though broader biotechnology development programmes show promise for creating the infrastructure and workforce needed for a more resilient food system, dedicated funding to increase consumer appeal and availability of new protein sources is necessary to build a futureproof food system,” the authors of GFI’s policy report noted.