European Plant-Based Sales Grow By 3% As Price Gap with Meat & Dairy Narrows

Sales of plant-based meat and dairy in Europe rose 3.3% in 2025, driven by affordable products that meet consumers’ taste expectations.

The plant-based market is firmly in ascendance in some of Europe’s major markets, thanks in large part to products that are closing the taste and price gap with animal proteins.

New research from the Good Food Institute (GFI) Europe, based on Circana data, shows that sales of meat and dairy alternatives in the six largest European markets reached €4.75B in 2025, up 3.3% from the year before.

In most cases, the growth was linked to expanding volumes of plant-based food. As in 2024, Germany, Italy, France, and Spain all saw sales rise last year, while the UK and the Netherlands experienced declines.

The report includes data on sales of traditional plant proteins like tofu, tempeh and seitan, but these figures aren’t included in the overall totals, as they’re not marketed explicitly as analogues of meat.

Even as animal-free options were generally more expensive than conventional meat and dairy, the price difference has shrunk. That said, the continued dominance of branded products in most countries outlines consumers’ preference for taste and quality, a key driver of plant-based sales.

“While the price gap with animal products is closing in many categories, affordability alone is not sufficient for growth – a good eating experience is also crucial to reach larger audiences,” said Helen Breewood, senior market and consumer insights manager at GFI Europe.

“To help Europe shift towards a more sustainable, resilient and healthy food system, companies and governments need to invest in research to improve taste and texture and build the infrastructure needed to scale production,” she added.

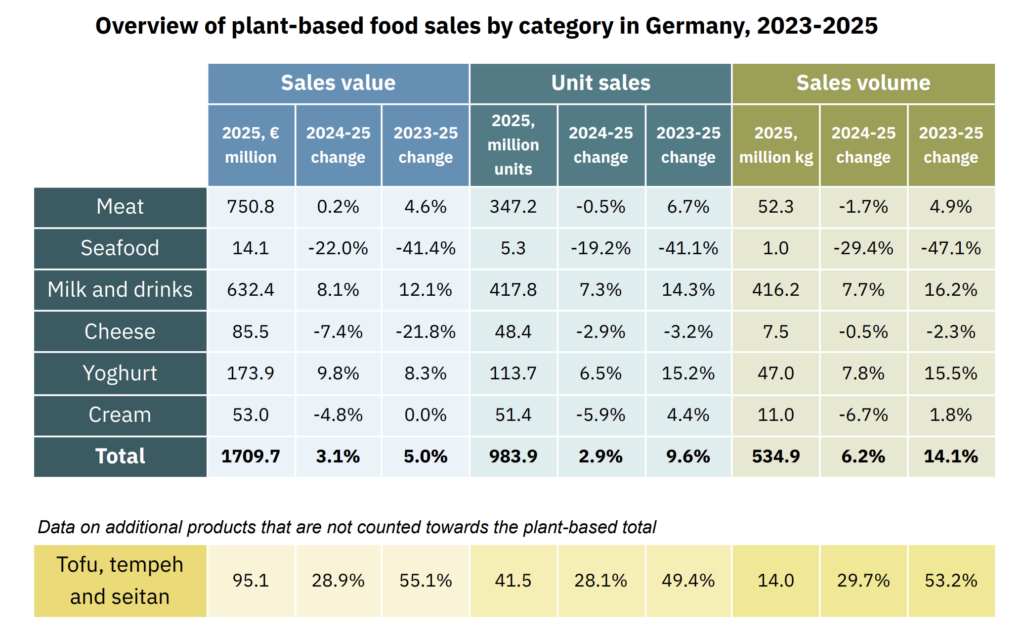

Germany rides on cheaper-than-dairy plant-based milk

Germany remained the leading European market for plant-based food, with year-on-year sales up by 3%, totalling €1.7B. It accounts for 36% of the sales across the six countries analysed in the report. Volume sales, meanwhile, climbed by 6%.

GFI Europe ascribes this partly to more affordable private-label offerings, a recovery in branded product sales (up 3.5%), and the success of plant-based milk.

Milk alternatives saw an 8% increase in sales and accounted for 9% of all milk sold in German supermarkets last year. They were bought by 38% of households, one percentage point above 2024.

On average, they were 10% more expensive than cow’s milk, largely because they are charged a 19% VAT rate (versus 7% for dairy). Still, in terms of private-label products, plant-based milk ended up cheaper than its conventional counterpart.

Vegan meat alternatives didn’t enjoy the same success, with their sales levelling off with a 0.2% year-on-year gain, although this total was a 4.6% improvement on 2023. Their household penetration dropped by two points to 31%, and volumes were down by nearly 2%.

Some categories saw sales declines, including plant-based seafood (-22%), cheese (-7%), and cream (-5%), though purchases of non-dairy yoghurt grew by 10%. Tofu, tempeh and seitan collectively enjoyed a 29% boost, but the volume sales of meat alternatives were still 3.7 times higher than these proteins.

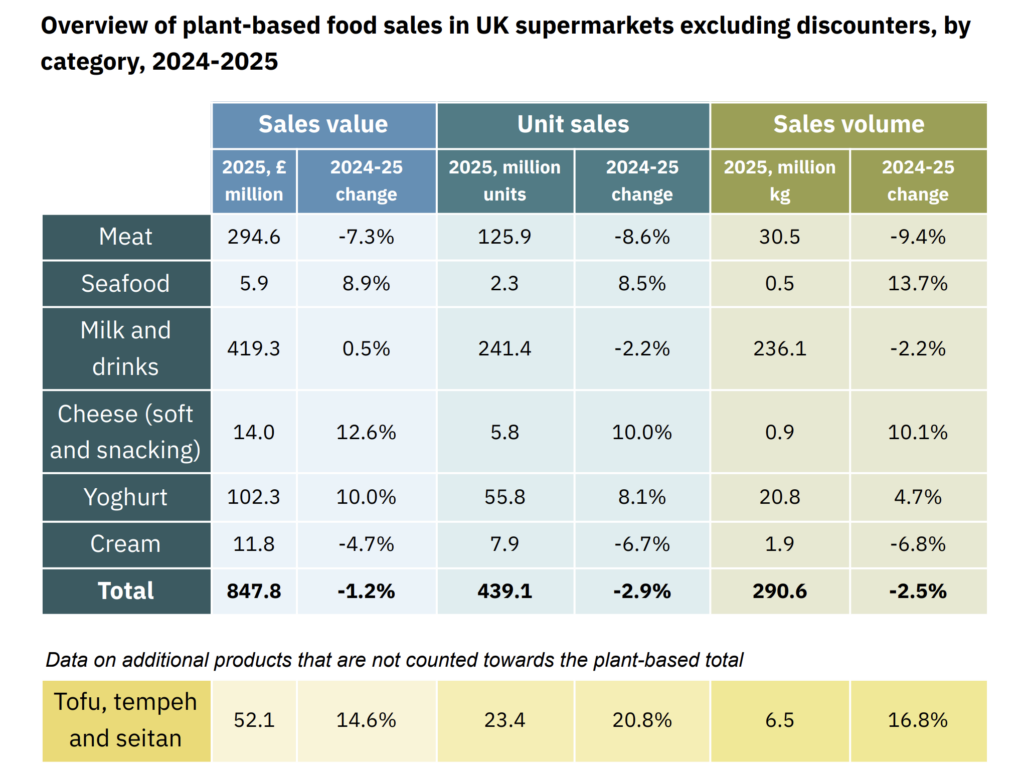

UK puts trust in branded, taste-first plant-based products

Plant-based food sales in the UK contracted slightly by 1% to €993M, with volumes down 2.5%, as the ultra-processed food (UPF) debate continued to shape Brits’ dietary decisions.

Value sales of meat alternatives fell by 7%. It’s worth noting, though, that Circana’s analysis does not cover discounters like Lidl and Aldi, whose proportion of sales increased between 2023 and 2025, according to NIQ Homescan data. “So the sales figures presented here may overstate the contraction of the plant-based meat category,” GFI Europe outlined.

Plant-based milk flatlined with a 0.5% uptick, where premium barista-edition milks saw a 10% uplift, underlining the importance of taste and performance among Brits. This can also be seen in the gulf between branded and private-label products – the latter make up 90% of vegan food sales in the UK.

Meanwhile, dairy-free cream sales were down by 5%. Things were positive for vegan seafood (up by 9%), non-dairy cheese (13%), and plant-based yoghurt (10%).

Further, sales of tofu, tempeh and seitan improved by nearly 15%. Despite the whole-food wave in the UK, non-analogue meat alternatives like bean burgers saw an 11% decline in volume last year. In fact, the sales volume of plant-based meat was 90% higher than that of these categories combined, again showcasing the appeal of premium products that offer taste, texture or formats similar to animal protein.

Moreover, the share of households that purchased plant-based milk in 2025 rose by 1 point to 38%, while penetration for meat alternatives fell by 2 points to 31%.

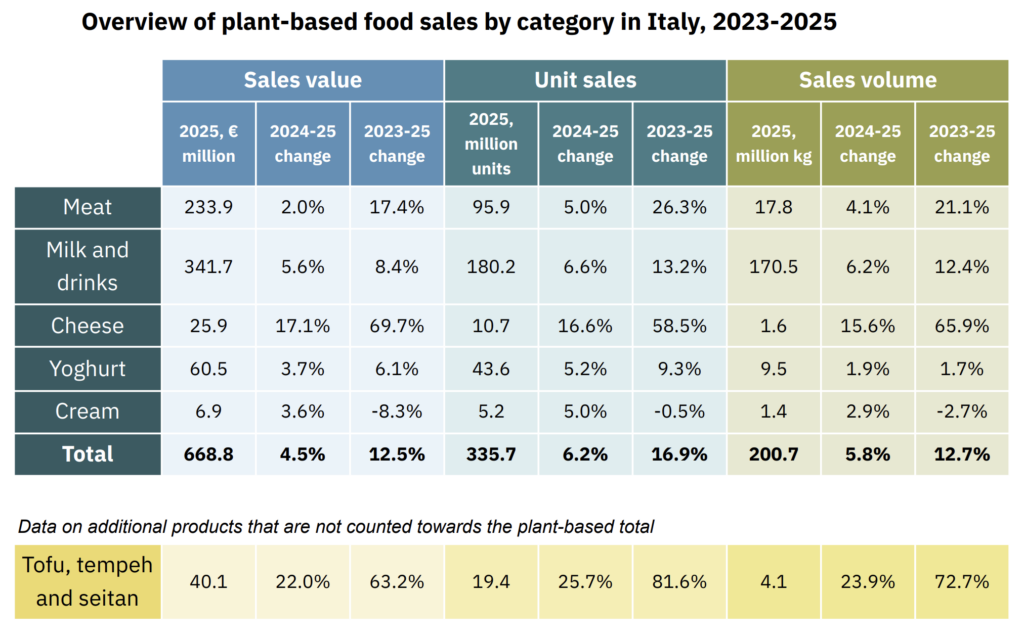

Italy enjoys growth in every plant-based category

Italy was among the only two markets where each product segment experienced an uptick in sales, totalling €669M, a 4.5% hike from the previous year; sales volume increased by 4%.

Plant-based milk was the dominant category, accounting for over half of the country’s plant-based market and posting a 6% rise in retail sales. These products account for 8.5% of all milk sold in Italy.

Sales of meat alternatives were up by 2%, too, though the growth was much slower than the 15% increase recorded between 2023-24. Vegan yoghurt and cream observed a 4% hike each, with dairy-free cheese remaining the smallest yet fastest-growing category in Italy with a 17% increase.

This performance has been driven by falling prices for plant-based meat (-3%) and milk (-1%). Meanwhile, dairy-free cream is 19% cheaper than the conventional version.

Notably, private-label products are growing faster in volume (+20%) than branded options (+7%), but the latter still account for 65% of the market. Tofu, tempeh and seitan, meanwhile, sold 21% faster last year.

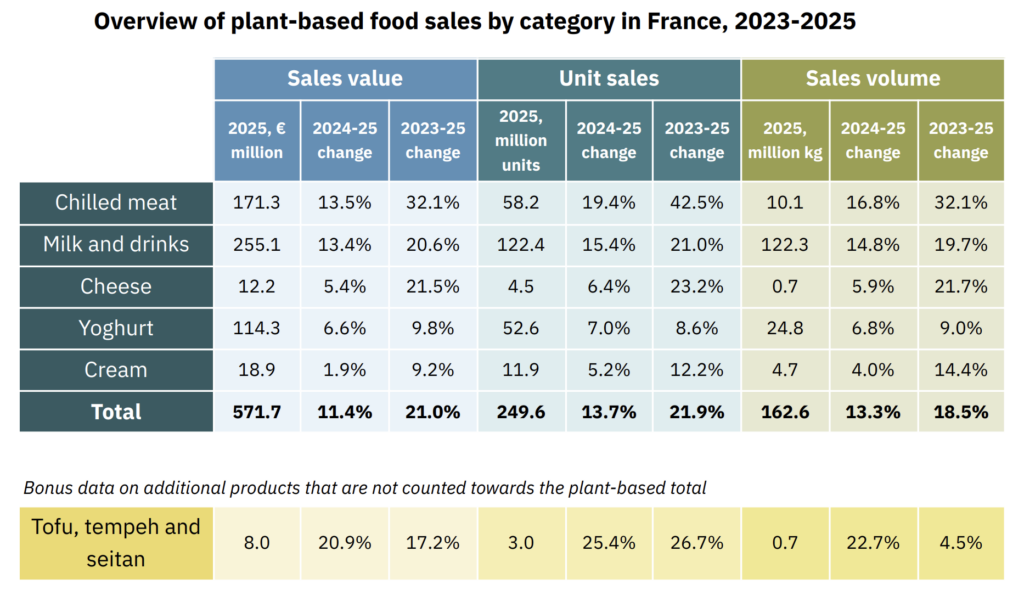

France is Europe’s fastest-growing plant-based market

France was the other country that observed growth in each plant-based category analysed. Sales reached €572M in 2025, 11% higher than the previous 12 months – that’s faster than any of its European counterparts in the report.

It is the only market where meat alternatives saw the biggest uptick, with sales up 13.5% and volumes up 17%. This was largely thanks to a near-3% reduction in the average price of these products.

Still, plant-based milk was the leading category, chalking up 13.4% rise in supermarket purchases. That said, this is still a young market, and milk alternatives captured only 5.5% of the overall milk market. This fell to 2% for chilled meat.

GFI Europe underscored the importance of reaching price parity: vegan meat products, despite cost reductions, are still 25% more expensive than animal proteins, and non-dairy milk is 68% more expensive.

Other vegan analogues that experienced a bump included cheese (5%), yoghurt (7%) and cream (2%). Tofu, tempeh and seitan represented the smallest segment, but their sales spiked by 21%.

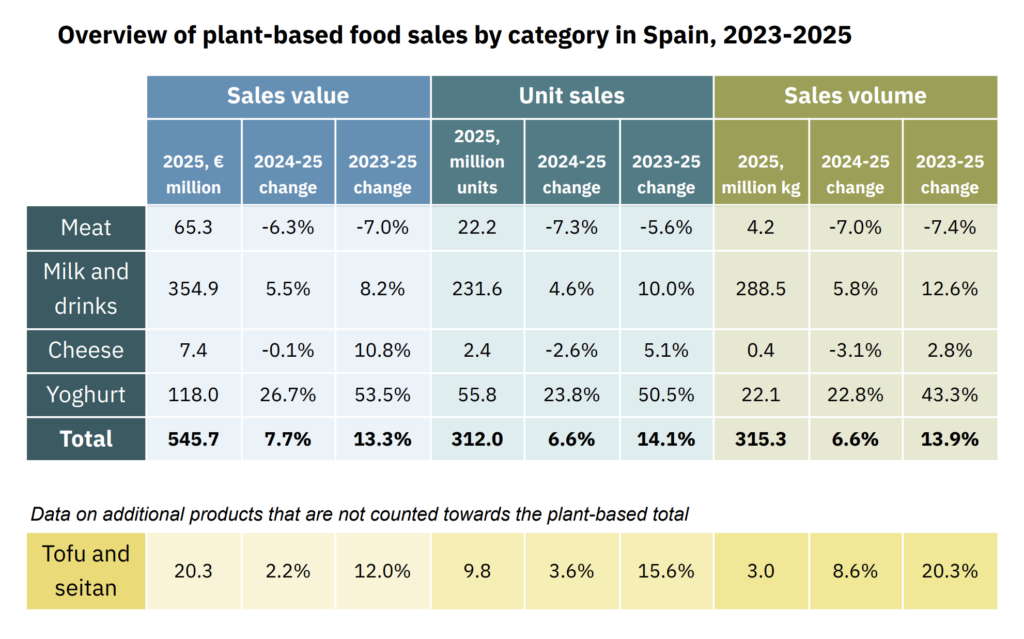

Spain sees plant-based milk in more households than the rest

Non-dairy products drove the plant-based category’s performance in Spain, where sales totaled €546M, a 2% increase. Volume sales grew 7%.

Plant-based milk was the catalyst, contributing to 65% of the market. These sold 5.5% faster in 2025, making up 10% of all milk sales, and were purchased by nearly half (48%) of the country’s households. The success was driven by private-label offerings, which only cost 7% more per litre than cow’s milk, as well as innovative barista milks.

Vegan yoghurt grew even more quickly, with a 27% growth in value sales, making up 22% of Spain’s plant-based analogue market. Non-dairy cheese flatlined with a 0.1% decline, while tofu and seitan saw a 2% rise (much slower than the rest of Europe).

Meat analogues suffered the most, as purchases slowed by 6% and volumes dipped by 7%. GFI Europe blamed their high prices, given that they cost twice as much as conventional meat. Only one in five Spanish households (19%) bought these products last year, a two-point decline from 2024.

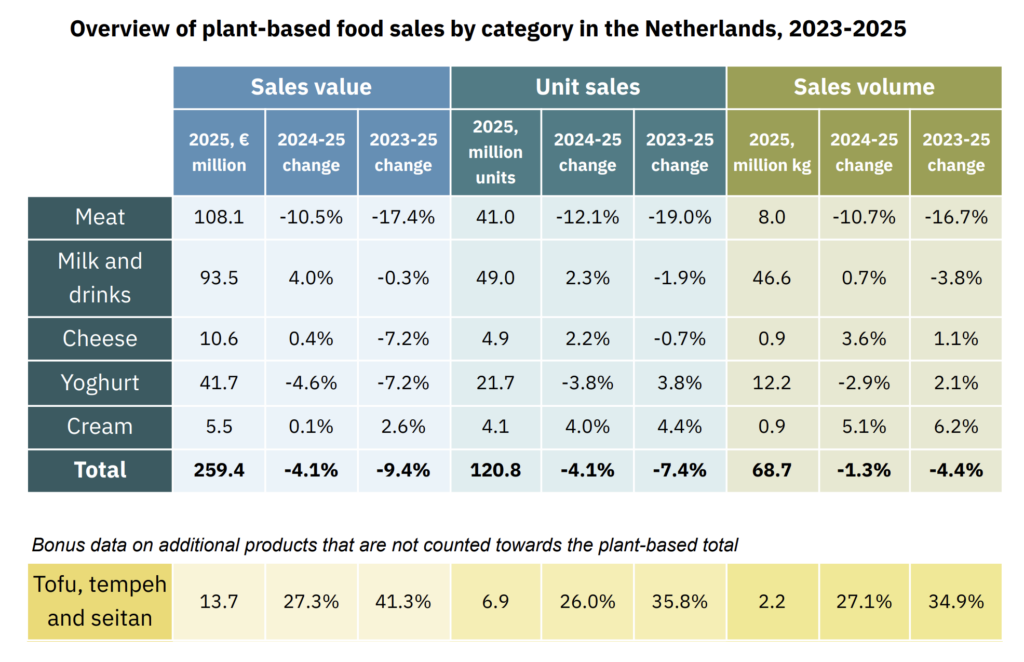

Netherlands remains smallest plant-based market in Europe

Despite its retailers leading the protein transition with sales rebalancing pledges, the Netherlands witnessed a 4% drop in overall sales of plant-based food, which totalled just €259M.

This was largely thanks to a 10.5% decrease in purchases of plant-based meat, the largest segment in this market, driven by a 16% dip in sales of branded meat alternatives, though the country’s foray into blended meat could have played a role here too.

Tofu, tempeh and seitan were increasingly popular in the Netherlands, with a 27% spike, the second-highest in Europe. Affordability is a key factor here – tofu costs around a third as much as branded plant-based meat.

Even then, Dutch consumers bought the latter 3.6 times more than these three traditional plant proteins combined, confirming that products mimicking the taste and format of meat retain the broadest appeal.

Sales of non-dairy yoghurt fell by 4.5%, and the performance of cheese and cream alternatives levelled off with increases of 0.4% and 0.1%, respectively.

Meanwhile, Dutch consumers spent 4% more on plant-based milk, which represented 9% of the overall milk segment. Here, too, rapid growth in premium categories like barista milk suggests that better product performance can drive sales.

More investment could unlock taste and price parity

GFI Europe noted how most plant-based products are closing the price gap with animal proteins, which has, in most cases, been associated with volume growth. There are exceptions where premium products have outperformed cheaper options.

“This shows that both taste and price are important to consumers, and for further growth, products must not require consumers to compromise on either,” the think tank said.

“Further investment in research, innovation and manufacturing capacity is essential to close those gaps. Governments and the food industry can support progress by investing in research to improve taste and texture, and building the infrastructure needed to scale production and lower prices.”

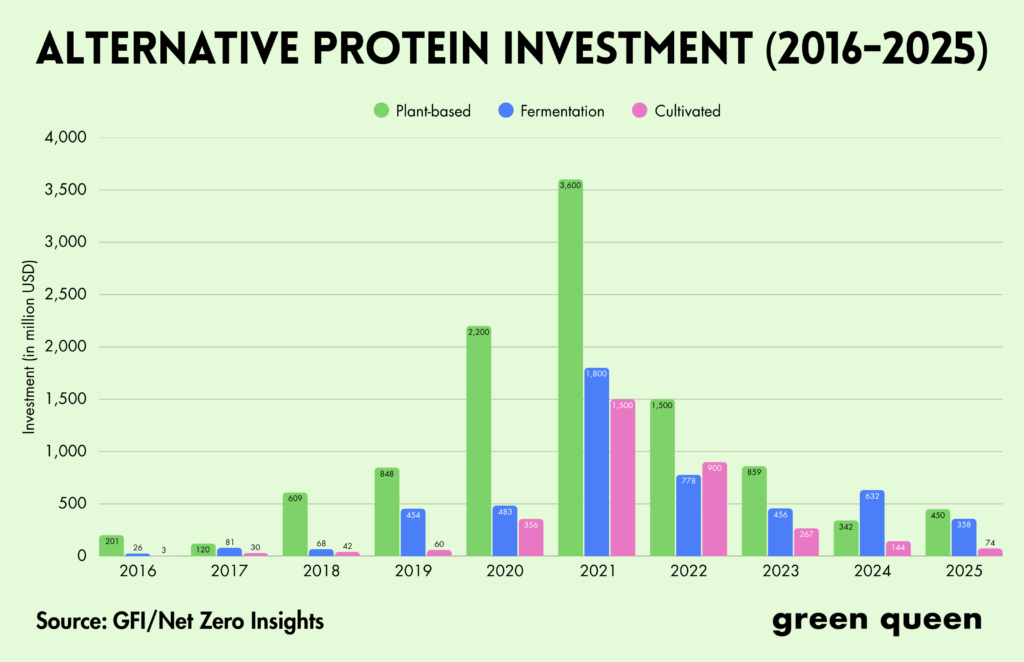

Last year, funding for plant-based companies climbed by 31.5%; this was largely due to Beyond Meat’s $100M round. Without it, funding for the category would have only increased by 2%.

However, data from French consultancy DigitalFoodLab paints a murkier picture for the larger agrifood tech sector in Europe, investment in which declined by 25% in 2025. That said, the region now makes up 28% of the global total, and while investors are shifting away from alternative proteins internationally, Europe is “building strong positions in key technologies” in this space.