When It Comes To Alternative Proteins, Australia is Punching Above Its Weight, Argues Food Frontier’s Simon Eassom

Australia has become a global leader in alternative proteins, says Food Frontier’s Simon Easson, with the country witnessing a surge in innovation, government support, and market strategies. From shifting policies to groundbreaking technologies, the Australian smart protein sector is booming.

Whilst nobody has been immune to the challenges arising from geopolitical and financial issues of the past two years, Australia has fared better than most, with alternative proteins beginning to gain traction at the federal and state level: more than 26 government-authored or funded papers now feature alternative proteins in their discussions – a topic that was largely absent from government policy before 2018. Foodservice, especially, has bucked the trend with Food Industry Foresight’s Sissel Rosengren reporting sector growth at Food Frontier’s AltProteins23 conference.

Food Frontier’s 2020 State of the Industry report projected that plant-based meats alone could generate nearly AU$3 billion in Australian sales and provide 6,000 full-time jobs by 2030. The Australian government’s Commonwealth Scientific and Industrial Research Organisation (CSIRO) further projected that the broader plant protein sector, including dairy milk alternatives, bakery ingredients, and protein products used in sports nutrition, could deliver an additional AU$3 billion (totalling AU$6 billion) and that precision fermentation presents an AU$1.45 billion domestic opportunity by 2030. While there is no Australia-specific projection at this stage, McKinsey & Company estimate the global cultivated meat market to be worth US$25 billion by 2030.

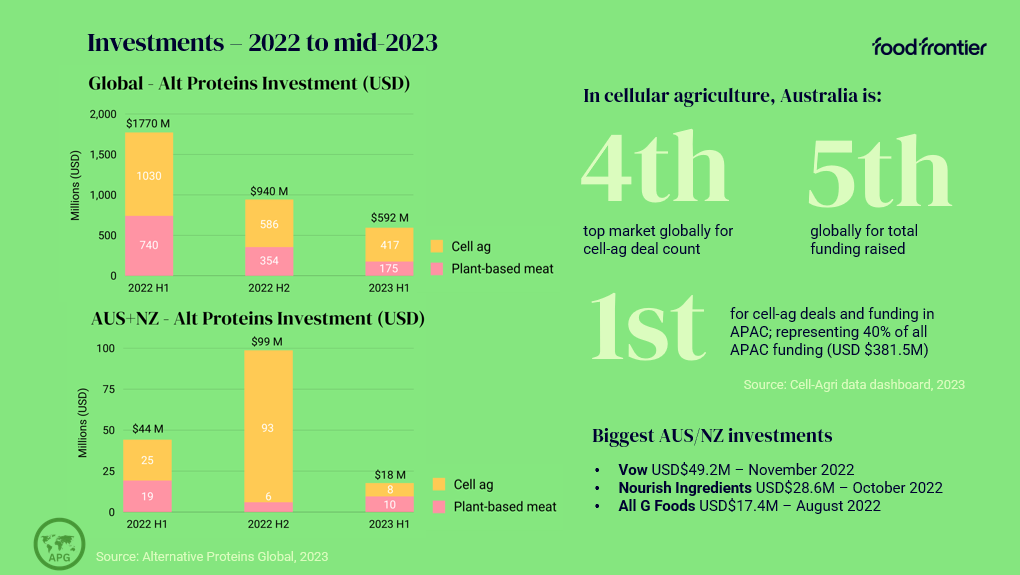

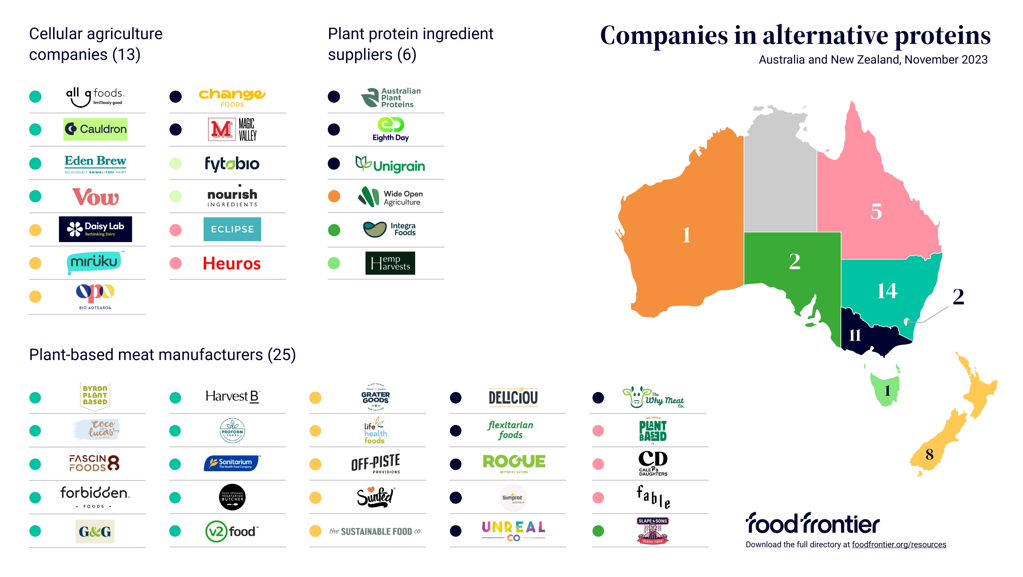

According to Alternative Proteins Global data (see graphic above), Australia ranks eighth globally for total alternative protein investment from 2022 to the end of June 2023. Moreover, it is the fourth top market globally for cellular agriculture based on deal count and the fifth for direct cellular agriculture investment with US$176 million raised. The number of alternative protein companies in Australia has risen from fewer than five in 2017 to more than 30 in 2023 and, of the 300 products now available on our supermarket shelves, 56 per cent are made by Australian plant-based meat manufacturers.

Recognising the scale of the broader plant protein opportunity, the number of plant protein ingredient manufacturers in Australia has increased to at least six and is growing. Made from Australian-grown grains and pulses, these value-added products are now being used by domestic and international companies across more than 23 different food and beverage categories to deliver increased protein and fibre content. Start-up innovators, such as Eighth Day Foods and Whole Green Foods, have achieved significant technology breakthroughs with strong interest shown by multi-national food manufacturers: Eighth Day with its ‘Rapid Solid-State Fermentation’ process re-defining the game in affordable and sustainable plant-based protein production and Whole’s ‘Whole Ingredient Nutrient Extraction’ (WINX) utilising ultra-high pressure to efficiently ‘explode’ the cells of the input ingredient, significantly enhancing the nutritional value and making it more bioavailable.

There are now nine domestic cellular agriculture companies, and Australia is on the verge of having its first cell-cultivated ‘meat’ product approved for domestic sale: Vow Foods’ novel foods application for cell-cultured Japanese quail as a food ingredient is currently before Food Standards Australia New Zealand (FSANZ). Food Frontier anticipates that Eden Brew will be submitting its application to FSANZ in 2024 for precision fermented dairy products, and is looking to release its dairy-free ice cream into retail outlets before the end of the year.

Against this backdrop, it is clear that several trends and growth strategies are emerging that will drive increasing adoption of alternative proteins across the food sector. Many of these can be seen across the globe but Australia is at the forefront of their development, as many ecosystem players and insiders shared during Food Frontier’s October 2023 conference.

- Producers, manufacturers, and service providers are beginning to take an ‘outside-in’, rather than an ‘inside-out’ approach.

To begin with, investments and advancements have been driven by the innovators developing a ‘good idea’ with limited reflection on consumer demand and market requirements. Promising signs show that providers are modifying their packaging, messaging and marketing. For example, menus in quick service restaurants are providing more plant-based options with descriptions focusing on ingredients and taste rather than labelling as vegan. Manufacturers are emphasising nutritional credentials rather than focusing exclusively on meat-free and animal-friendly credentials. - Foodservice is increasingly being seen as the lead environment for consumers’ first experience of plant-based meats, according to Mark Field of Prof Consulting Group.

That experience needs to be both a good one and repeatable, encouraging consumers to seek out future experiences, as well as identify the products they’re consuming for their own purchase and home cooking. Attracting first-time trialists via retail has been limited to those already consciously consuming for environmental or health reasons with few ‘curious’ consumers being converted.

Some restaurants, such as Brother Bon in Melbourne’s suburbs, base the entirety of their extensive menu on alternative proteins and focus on the Asian food styles on offer that can be enjoyed by an entire group of diners, meat eaters or otherwise. Promoting this approach, Harvest B, an Australian B2B alternative protein food technology business, has invested in chef training to facilitate the adoption of plant-based meats into institutional catering for hospitals, schools, prisons, armed forces establishments, and aged care facilities. FoodBuy, the sole sourcing partner of major foodservice player, Compass Group Australia, has seen business grow 800% in 2023. - These two aforementioned points have demonstrated the need to meet consumers “where they are”. One indisputable fact is that the vast majority of consumers are solely interested in tasty, affordable food with little motivation to compromise on those factors. A small percentage of consumers are interested in novel foods for their own sake.

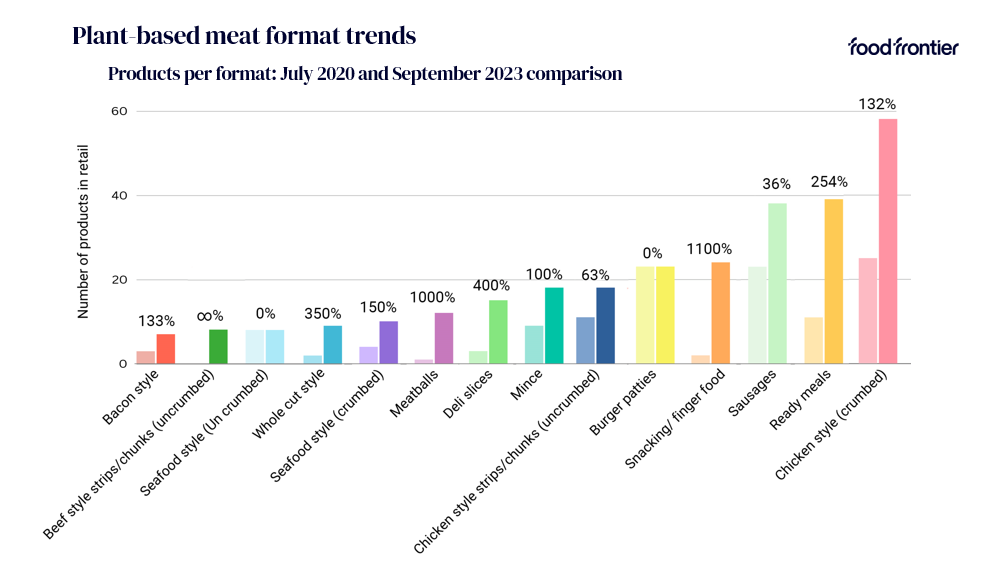

The impact of this factor is most apparent in the utility foods sector, with the market bombarded in its early years with multiple manufacturers of burgers, sausages, meatballs, nuggets and other finished products. The market has inevitably corrected itself and fewer players now dominate retail shelves in Australia. v2food, a partnership between Jack Cowin’s Competitive Foods Australia and CSIRO’s Main Sequence, enjoys a near monopoly in the major food supermarkets for chicken-style products (such as schnitzels, dippers, and nuggets) and its burgers and sausages. v2food’s burger has enjoyed growing sales as the plant-based meat offering at Australia’s fast-food equivalent of Burger King: Hungry Jacks. Cale Drouin’s manufacturing operation, Cale & Daughters, has moved towards making products under license to supplement its growing range of deli meats and dairy products sold under different brand labels. Diem Fuggersberger’s food business, Coco & Lucas, makes ready meals using its own ingredients as well as those of other manufacturers, such as Quorn.

Further partnerships forthcoming in 2024 reflect the increasing recognition for collaboration and inputs from ‘world’s best’ suppliers, rather than manufacturers attempting everything from end to end. The net result will be fewer, but better quality, choices for consumers such as a “planet burger” using 10-15% cultured meat with precision fermented fats, new algae-derived binders replacing methylcellulose, and a plant-based protein (such as mycelium) providing the increased umami flavour and texture. Several companies in Australia are actively forming these partnerships. - By far the biggest single growth impact for the alternative proteins sector will come from the ‘normalisation’ of these foods. The best example of progress to date comes from the precision fermentation of casein dairy protein for the manufacture of cheese and the advancements made by Dave Bucca’s Change Foods and the start of large-scale production of mozzarella in import-dependent countries such as the United Arab Emirates.

Global cheese production exceeds 20 million tonnes, trebling over the last 50 years, and driven largely by the obsession with pizza (Americans consume more than 3 billion pizzas per year). Precision-fermented mozzarella will soon become more readily available and cheaper than dairy-farmed mozzarella. As the cheese topping on pizza, this alternative protein (identical in taste and texture) will simply be ‘cheese’ with no need for customers to make choices based on environmental or animal welfare concerns. Likewise, the use of precision fermented eggs for scrambled eggs, omelettes, sauces, and in baking will also become normalised.

Australia has navigated global challenges adeptly, witnessing a remarkable surge in alternative protein adoption. Government support, a thriving foodservice sector, and a burgeoning industry indicate a promising trajectory. We stand at the forefront of shaping a sustainable and diverse future for the alternative protein sector. Food Frontier looks forward to releasing its State of the Industry report in mid-2024 which will demonstrate the current position and outlook for the next 10 years.