56% of Americans Open to Trying Novel Protein Ingredients, With Some Willing to Pay Four Times More for Them

Americans are willing to try novel proteins – including those that are plant-based, fermented or fungi-derived – with more than half happy to pay more for them than animal proteins, according to a new survey, which shines light on the importance of health in the US.

Lately, a lot of the messaging from plant-based brands has been centred around health. Impossible Foods and Beyond Meat – two of the industry’s giants – have rejigged their marketing strategies to focus on nutrition, just as Unilever is hoping to capitalise on the Ozempic boom by doubling down on gut health with its vegan portfolio.

These companies are playing to consumers’ demands, with one poll from last year suggesting that health is the main factor behind Americans eating meatless diets, after six in 10 cited it. In a post-pandemic world, nutrition is top of mind for consumers, and this can be evidenced in a new survey by McKinsey, which gauged 1,517 Americans’ opinions on novel proteins.

The poll found that a majority of Americans are open to trying new ingredients and over half are willing to pay more for them. But the way they respond to labels, and the products they really are happy to shell out more for, exhibit the importance of health in their food purchasing decisions.

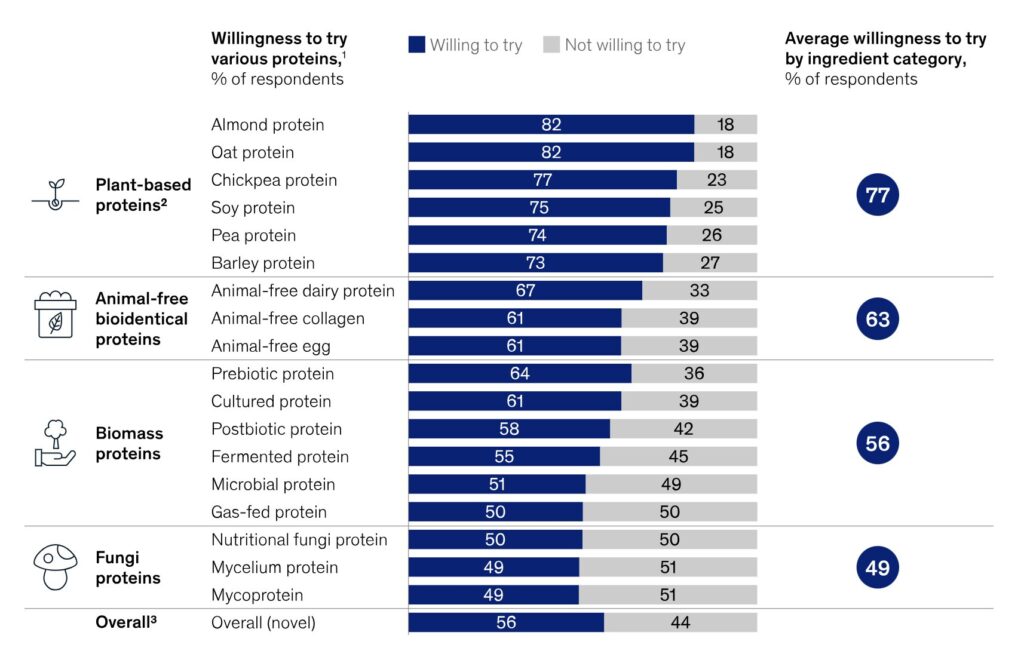

McKinsey identified 12 novel protein categories and classed them into three groups for the survey. Animal-free bioidentical products comprised precision-fermented dairy proteins, collagen and eggs; biomass proteins consisted of prebiotic, cultured, postbiotic, fermented, microbial and gas-fed ingredients, and fungal proteins included nutritional fungi protein, mycelium protein and mycoprotein.

The research also looked into plant-based ingredients like almond, oat, chickpea, soy, pea and barley proteins, but they were not the main focus, as they’re already established in the market

Over half of consumers willing to try novel proteins

Depending on the ingredient, between 49-67% of consumers are willing to try food or drinks that contain novel proteins, with animal-free dairy and biomass-fermented prebiotic proteins garnering the most support. In fact, 63% of respondents are open to trying precision-fermented products, and 56% said the same for biomass fermentation. This drops to 49% for fungal proteins, making up an average of 56% acceptance across the three categories.

In contrast, 77% are happy to give products with plant proteins a go, with almond and oat proteins being the most popular (82% each), followed by chickpea protein (77%), which trumped soy (75%) and pea (74%).

On average, 28% of respondents are more willing to try a novel ingredient if it makes the product healthier, with those aged 18 and above showcasing the highest degree of importance for health. For older demographics, however, taste is the most crucial aspect for acceptance of these ingredients. But unwillingness to try such products stems from a lack of awareness or questions about how these are made, with taste, naturalness and price also key. People who make over $100,000 a year expressed greater doubt (33%) about the long-term health effects.

Sustainability and health speak louder than ‘vegan’

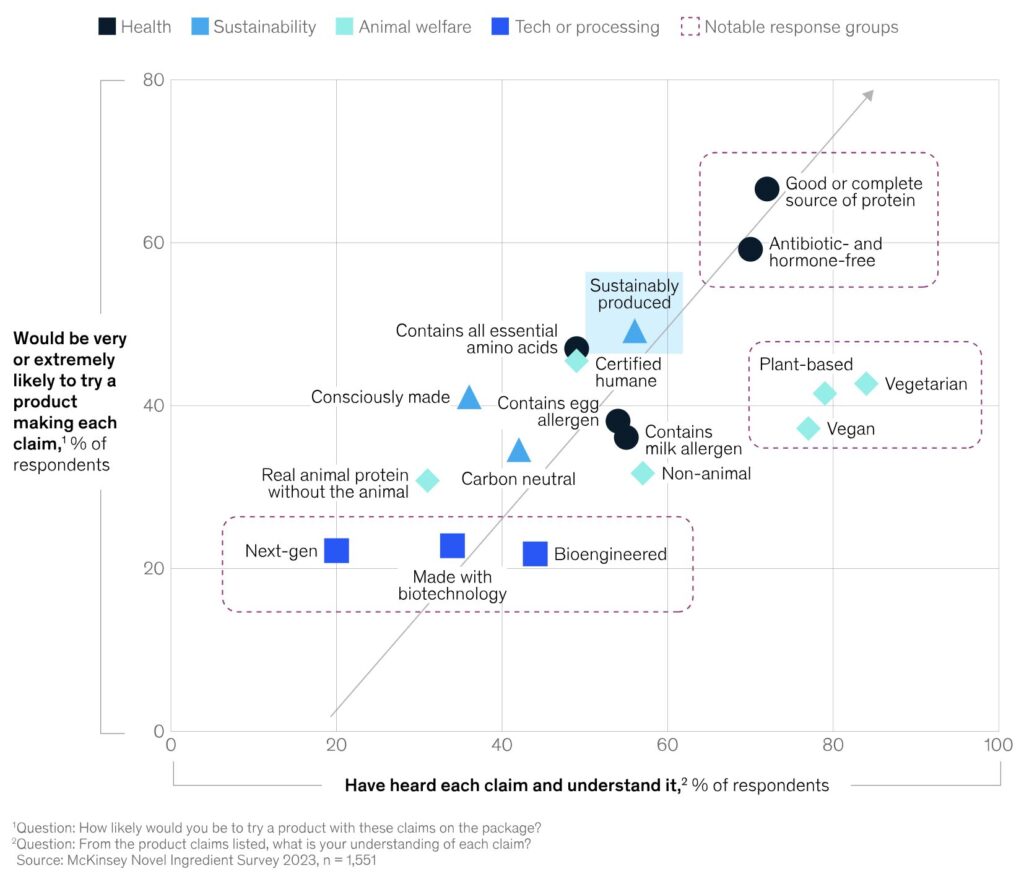

There has been tons of research about the best way to label vegan food on product packaging, with a dislike of the word ‘vegan’ being apparent globally. McKinsey found that familiar terms and well-understood nutritional statements like ‘good or complete source of protein’ or ‘antibiotic- and hormone-free) are the most compelling. ‘Sustainably produced’ is similarly impactful.

But while consumers understand words like ‘vegan’, ‘vegetarian’ and ‘plant-based’ well, these don’t significantly drive the trial of products. Even less effective are terms that indicate production methods, such as ‘bioengineered’, ‘made with biotechnology’ or ‘next-gen’, which highlights the neophobia associated with food tech.

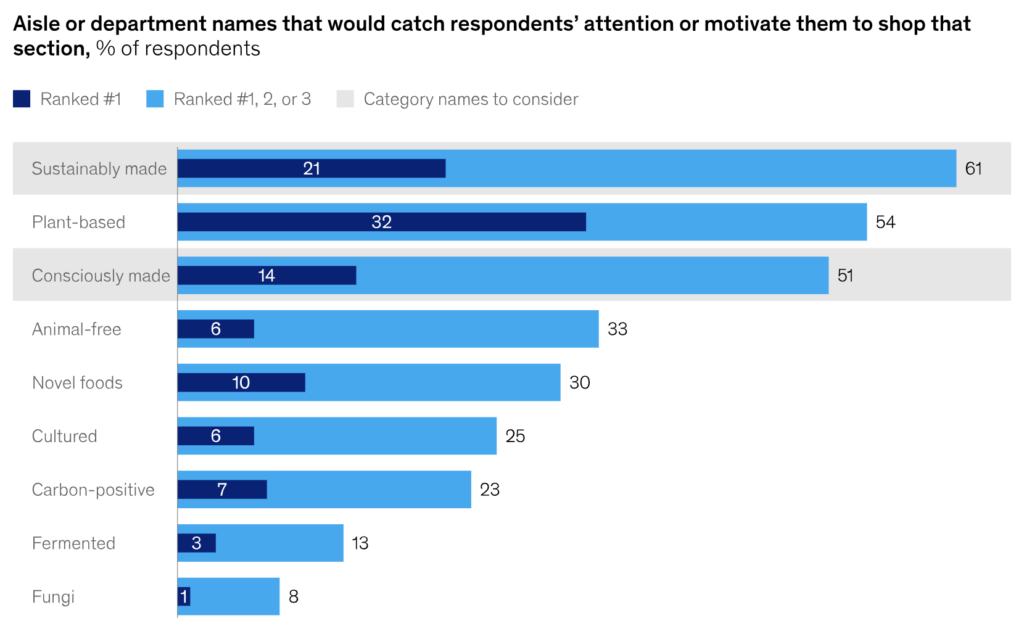

The survey also tested various names that could represent novel product aisles or sections in supermarkets. While ‘plant-based’ was ranked top by the highest number of Americans (32%), the most popular term overall was ‘sustainably made’ (ranking in the top three for 61% of respondents, versus 51% for ‘plant-based’. McKinsey earmarked this and ‘consciously made’ (in the top three for 51%) as category names to consider, while retailers should stay away from terms like ‘fermented’ or ‘fungi’.

Americans would pay more for novel proteins – lunch and snacking are key

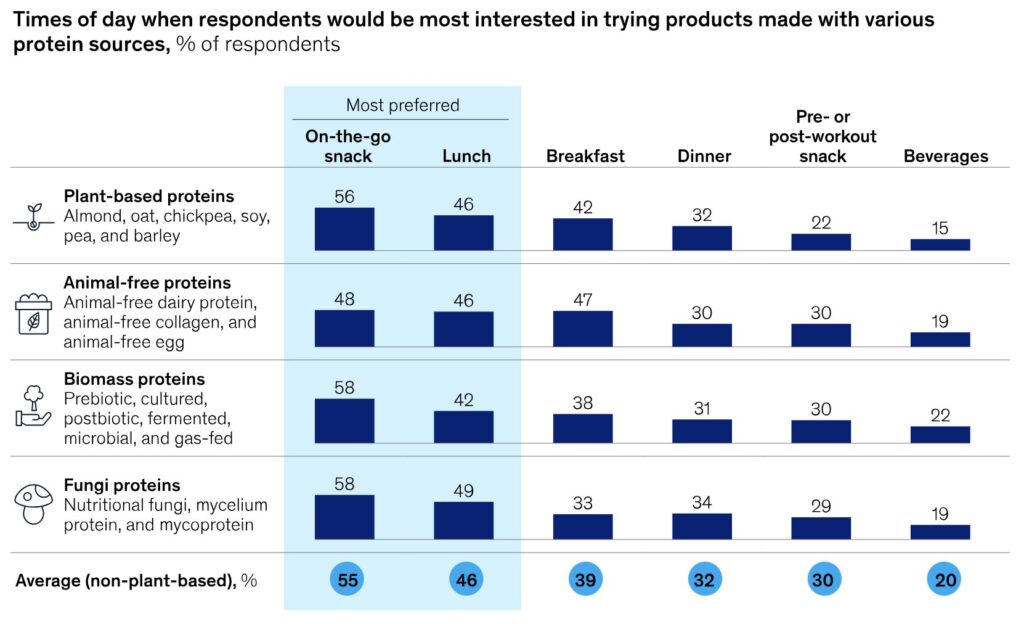

Respondents displayed much greater openness to try novel foods at lunch (46%) or in on-the-go snacks (55%) than breakfast (39%) or dinner (32%). McKinsey suggests that product development may benefit from a spotlight on the former two, with a lower focus on breakfast, and potentially avoiding centreplate dinner proteins.

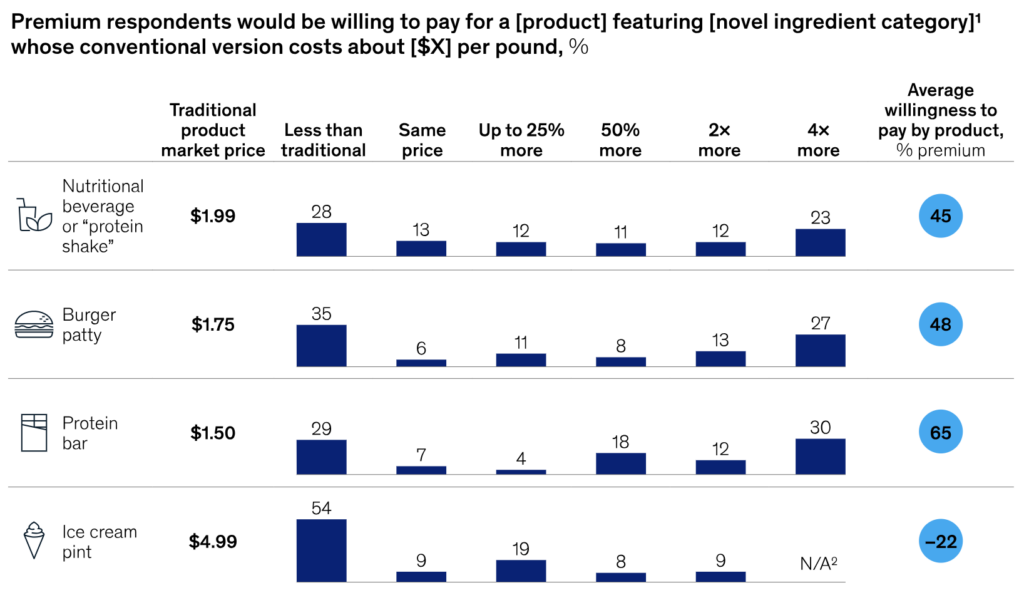

And in what may come as a surprise to some, more than half of consumers are happy to pay more for products whose animal-derived counterparts cost less than $2. For nutritional beverages like protein shakes, 58% are willing to pay between 25% and four times more, which rises to 59% for burger patties, and 64% for protein bars. Respondents were less open to shelling out more for products like ice creams, sandwiches or cookies.

In terms of channel, they were more receptive to paying more for retail and CPG products than in foodservice settings, which is interesting given that out-of-home consumption has been a crucial driver for meat analogue consumption. People’s willingness to pay for novel proteins didn’t vary significantly across ingredient types, however.

Key takeaways for novel protein producers

McKinsey highlights that many of the novel proteins it polled Americans about haven’t been commercialised yet, but added that there are several considerations for companies and investors in this space.

First, investing in consumer education is vital, with fewer than half aware of novel ingredients, and uncertainty about production being the largest barrier to their adoption. The survey found that people are more likely to try products if they’re recommended by professionals like doctors or nutritionists (44%), or family and friends (27%).

The importance of the health-environment-taste trifecta cannot be understated either, with respondents feeling novel proteins should be healthier than conventional animal sources, and more likely to eat those that are. Plus, those that have a comparable flavour or desirable alternative to taste and texture can increase adoption.

Next, innovation should prioritise the end application and channel. If companies want more consumers to dig into novel proteins, they should consider launching products for lunch, snacking or breakfast, and blend familiar terminology like ‘a good source of protein’ with emerging language such as ‘sustainably made’.

Finally, despite varying levels of awareness and trial, there wasn’t a significant gap in willingness to pay based on ingredient type. Instead, this was more linked to the category than the type of protein. This signalled that the underlying technology might not be too tall a hurdle, even if it’s new to human consumption.