Deep Dive: What’s Driving the Consolidation Wave in Alternative Protein?

More than 80 alternative protein startups have experienced M&As, insolvency, or closures over the last two years – and investors and founders don’t expect this consolidation trend to stop.

”I think the next generation of food companies will be built through collaboration,” says Deniz Ficicioglu.

She’s the co-founder of BettaF!sh, an alternative seafood startup that was acquired by US firm Bayou Best Foods in June. That was among a plethora of consolidation deals that have shaped the future food industry over the last couple of years.

Analysis by Green Queen finds that since September 2024, at least 82 alternative protein businesses have been bought out or acquired, merged, fallen into some form of insolvency, or shut down.

In fact, consolidation has really ramped up in the last year – 54 of these instances have occurred in the last 12 months, representing a 35% increase from the September 2024-25 period.

For Ficicioglu, the timing of this surge makes sense. ”Investment into food and alternative proteins slowed significantly around 2023. Most startups had between 18 and 24 months of runway, so we’re seeing the consequences now,” she explains.

”Companies that couldn’t reach profitability, adapt their business model, raise additional capital, or find the right strategic partner are facing difficult decisions.”

It’s a view shared by investors active in the space, including Yoni Glickman, managing partner at PeakBridge, whose portfolio includes startups like Vow, Rival Foods, Imagindairy and Standing Ovation.

“Many of these companies raised in 2021 and 2022 and have reached the end of their runway. Investors are more interested in companies that have proven product-market fit and traction, as opposed to investing in an alternative protein vision that was overhyped over those years,” he says.

Christian Nagel, co-founder and partner at Earlybird, an investor in Parima, concurs: ”The sector is moving from a capital-abundant phase to one defined by execution and economics. Many companies were funded on expectations of rapid category adoption, but consumer demand, manufacturing scale, and margins have taken longer to materialise.”

Higher interest rates and shifting investor focus drive consolidation

Of the 54 deals announced since July 2025, nearly two-thirds (65%) have involved acquisitions, while the rest have seen companies enter insolvency, discontinue alternative protein brands, or cease operations altogether.

For Steve Simitzis, founder and managing partner of Replicator VC, you can track this back to when the US Federal Reserve began increasing interest rates. He views the collapse of Silicon Valley Bank and First Republic as the turning point away from the previous cycle.

”If we take 2023-24 as the beginning of the funding drought, many of these companies still have cash in the bank from their previous raise, and others raised bridges or found a way to run on fumes (for example, with layoffs and hard pivots),” he says.

”At some point, the money just runs out. If the typical startup round is capital for 18-24 months, plus a bridge for 12-18 months, that puts us at about 2025-26 for the big crashout.”

Nagel agrees that higher interest rates and a more selective funding environment have accelerated a ”necessary market correction, separating businesses with differentiated technology and commercial traction from those that relied primarily on growth narratives”.

Among the companies that have doubled down on M&As as a growth strategy is the Livekindly Collective, the owner of leading brands such as Oumph, Fry’s and Like. The firm recorded its first profitable month last year, and acquired Germany’s Greenforce earlier this month.

The company sees this as a sign of a maturing industry. ”Over the past decade, significant investment drove innovation and the launch of many new businesses. While that accelerated category development, it also created a highly fragmented marketplace,” explains CEO David Suarez.

”Today’s environment is different. Investors are focused on sustainable growth, profitability and operational discipline. At the same time, retailers are looking for partners that can deliver scale, reliability and category expertise. As industries mature, consolidation is a natural outcome as stronger business models emerge and companies seek greater scale and efficiency,” he adds.

”For us, M&A is not about getting bigger for the sake of it. It’s about building stronger businesses with the scale, capabilities and efficiencies needed to serve consumers and retail partners more effectively.

”Consolidation enables companies to combine complementary strengths, invest more effectively in innovation and operations, and create more sustainable businesses for the long term.

Where has all the money gone?

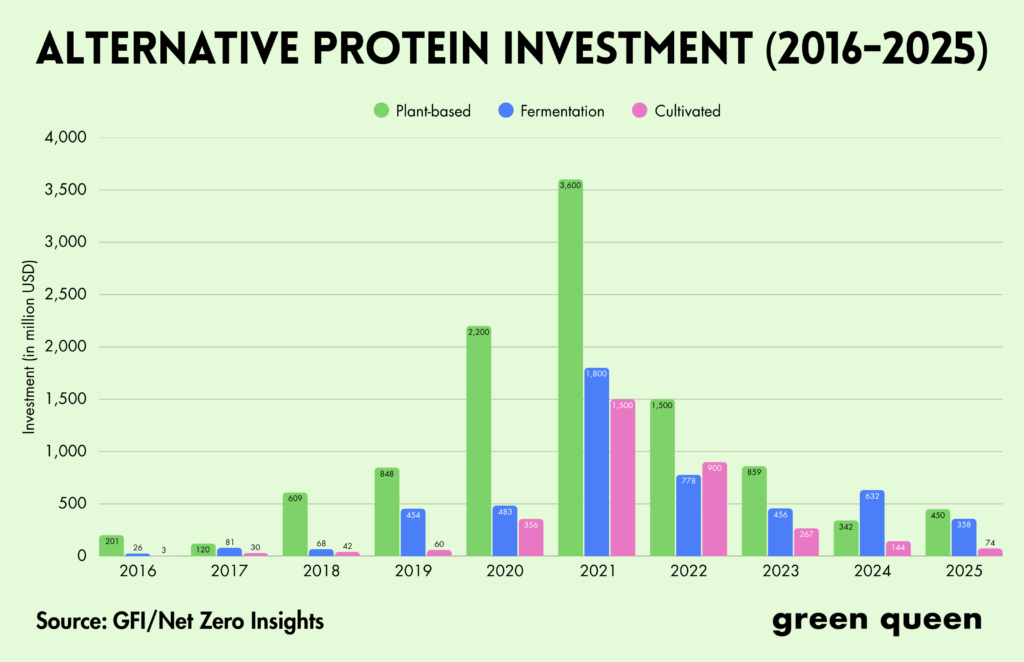

To put the funding issues into perspective, it’s worth noting that overall investment in the alternative protein industry totalled just $881M in 2025, falling below the $1B mark for the first time since 2018.

Fermentation companies experienced a 43.5% decline, while cultivated meat startups collectively raised more money in 2021 than in the following four years combined. Plant-based firms, meanwhile, saw a 31.5% increase from the 2024 total, but only because of Beyond Meat’s $100M debt financing round, without which this sum would have only increased by 2%.

”At the beginning of the decade, generalist VCs entered the space with unreasonable expectations around time horizons and exit scenarios. Similarly, the alternative protein bubble has largely burst due to both changes in consumer sentiment and overly hyped startups that were focused on a vision rather than proven product-market fit,” says Glickman.

The founders we spoke to agree that investors have become more selective. They’re prioritising strong fundamentals like ”profitability, cash generation, efficient operations and a clear path to sustainable growth”, according to Suarez.

”For plant-based food companies, the conversation has shifted from potential to execution. Investors want to see strong brands, differentiated products, consumer demand and disciplined business performance,” he says.

Ficicioglu feels the industry was too focused on trends and consumer hype, and not enough on solving real problems and building healthy businesses. To her, the shift in investor mindset is a positive development, as it could push founders to build businesses that consumers genuinely need, not just those that fit the current investment climate.

”We’ll see a different type of investor in food tech going forward: investors who understand the industry, think longer term, and want to build sustainable businesses rather than chase the next hype cycle,” she says.

The AI problem, and how alternative protein can win back investors

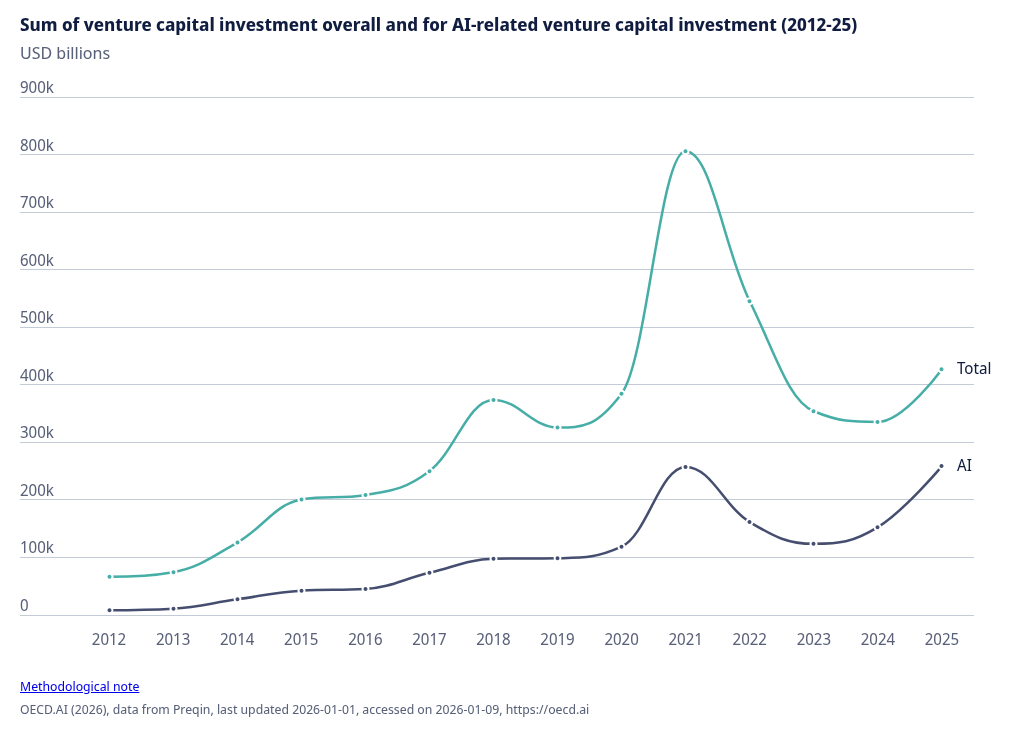

Investors point out that capital has become much more disciplined across the VC landscape, not just food tech. Pitchbook’s analysis shows that as of Q1 2026, VC fundraising in the US has fallen by 70% from its 2022 peak.

“Investors are now more aware of the long time horizons and capital intensity of synthetic biology. The companies that are fundraising successfully are those that have largely proven they can scale in capex-light scenarios, [and] have attractive unit economics and regulatory approvals,” says PeakBridge’s Glickman.

Nagel reiterates that investors today want “clear technical differentiation, defensible IP, capital efficiency and a credible path to profitability.” In that context, artificial intelligence (AI) has become the darling of the VC world, with firms in this space capturing 61% of global venture funding last year.

This is something future food firms can use to their advantage. ”AI is the unlock for alternative protein, period. You can develop better and cheaper products, faster. This reduces burn, and gets these companies commercial-ready with less capital than the previous wave,” says Simitzis.

”Technologies such as AI can certainly help improve areas such as forecasting, product development and operational efficiency,” notes Livekindly Collective’s Suarez. ”However, investors ultimately back businesses that deliver value to consumers and can create long-term sustainable returns. Technology can be a powerful enabler, but it is not a substitute for a strong business model.”

Along those lines, Nagel believes that just because AI attracts significant capital doesn’t mean other categories are uninvestable: ”Companies will continue to attract funding if they solve meaningful problems with proprietary technology and can show strong unit economics. The bar has simply become much higher.”

Simitzis suggests that validating scalability is ”merely table stakes”; proving consumer demand is the real key to attracting capital. ”Alternative protein startups need to identify a customer or segment (can be a B2B customer, or a consumer market, or government, etc.) with a burning need for your product,” he states.

”Not a ’sure, it would be nice to meet our ESG targets someday’ – that customer is just being polite. Find a burning problem that your alt protein product or technology uniquely solves for a customer who has money to spend.

”To identify these burning needs, we can start by looking at the fundamentals: food inflation is still hurting consumers; GLP-1 is increasing the demand for protein; developing nations are getting richer and demanding Western diets; [and] climate change is putting pressure on livestock.

”Even whey (a waste stream) is expensive now. All of these pressures happening at once is almost definitely creating business problems for food producers that alternative protein startups can uniquely solve.”

Are plant-based companies disproportionately affected by consolidation?

Plant-based food is the category most impacted by the consolidation craze, accounting for 72% of the M&A deals, insolvencies and closures since July 2025. In contrast, cultivated protein and fermentation-focused firms only accounted for 15% and 11% of the deals, respectively.

There’s a simple reason for this disparity: plant-based is the most mature and commercially established segment, and is home to far more companies than others.

”Plant-based brands already have retail distribution, manufacturing infrastructure, consumer awareness and established revenue streams, making them more attractive candidates for acquisitions and consolidation,” says Suarez.

”Many cultivated meat and fermentation businesses remain at an earlier stage of commercial development, with significant focus on technology scale-up, production economics and regulatory pathways.”

Nagel outlines how many plant-based businesses operate in crowded product categories with limited differentiation, which makes M&As and market exits more likely. He echoes Suarez by suggesting that the key challenges for cell cultivation and fermentation firms relate to scalability and regulation, not consolidation.

Still, Simitzis feels consolidation for the plant-based category is ”disproportionately higher”, explaining it as a ”difference in survival rates for startups with consumer models vs startups with B2B models”.

”The consumer market turned hard against plant-based, with the decline of Beyond Meat stock as the bellwether. Meanwhile, fermentation firms (especially in Europe) are finding traction as ingredient plays, selling into large food producers,” he says.

”And an increasing number of cultivated players are finding their own B2B pivots into adjacent industries like biopharma and beauty. So I would chalk it up to different business models, and consumer business models were hit hardest by food inflation and the general Trump-inspired backlash against plant-based.”

Suarez suggests the plant-based category is moving from fragmentation towards scale: ”The next phase of growth will be led by fewer, stronger players that can invest in innovation, serve retailers more effectively and create long-term value for consumers. Consolidation is not about reducing choice; it’s about building sustainable businesses that can help grow the category for years to come.”

Consolidation set to continue, as experts call it ’necessary and healthy’

The food tech experts we spoke to agree that consolidation in the alternative protein sector won’t slow down anytime soon. After all, this sector has seen seven acquisitions or liquidations since June.

”We expect consolidation to continue over the coming years. Retail shelf space is finite, competition remains intense and both retailers and consumers are increasingly looking for brands that can consistently deliver quality, innovation and value. We believe the sector will continue to evolve towards fewer, stronger players that are capable of driving long-term category growth,” says Suarez.

Ficicioglu strikes an optimistic tone, suggesting that as the trend continues, we’ll see a new generation of startups emerge: ”They’ll be leaner, more focused, and built around solving real customer problems from day one. That’s good for entrepreneurs, good for investors, and ultimately good for consumers.”

She views consolidation as a necessary phase for the industry, arguing that it brings together complementary expertise, technologies, and market access to create stronger companies with a higher chance of long-term success.

Glickman agrees, noting that many food tech startups have successfully developed innovative technologies or brands but deployed their capital inefficiently: ”Through combinations, overhead and opex costs can be deployed more efficiently, giving both founders and investors better outcomes. Investors who can successfully deploy rollup and integration strategies will be very interesting to watch.”

Both Nagel and Suarez call consolidation necessary and healthy. ”Most emerging industries go through a period of rapid expansion, followed by rationalisation as scale becomes increasingly important. Consolidation can help create stronger businesses with the resources to invest in innovation, manufacturing capabilities, consumer engagement and category development,” says Suarez.

“I see consolidation as a healthy and necessary step in the maturation of the sector. Every emerging industry goes through a period in which too many companies pursue similar opportunities, and eventually the strongest technologies, teams, and business models emerge,” outlines Nagel.

”I expect consolidation to continue over the next couple of years, although the pace will increasingly depend on improving financing conditions and consumer demand. Ultimately, a more focused ecosystem should create stronger companies capable of building lasting global businesses.”

’We need change from the top and the bottom’

Simitzis adopts more of a ”creative destruction is good” view, noting that consolidation isn’t ”good or bad or necessary”, but makes for a nice press story.

”Ultimately, it’s not press or social media that makes or breaks an industry. Besides, there are other paths for a failed company that continue to advance the space. Talent and IP can be rehomed,” he says.

”There are still some companies operating in a zombie state, so there are probably a few more in the pipeline. But eventually we’ll run out of companies that were forged in the days of free capital, and the pace [of consolidation] will naturally slow down.”

Ficicioglu strongly believes that companies come and go, but good ideas don’t, arguing that many current innovations will return when markets, regulators and consumers are ready for them.

It underscores why she decided to sell her startup to Bayou Best Foods. ”BettaF!sh has built a strong brand, unique products, and a recognised position in both the plant-based seafood category and the European seaweed ecosystem. When we met Bayou, we initially explored a collaboration, but it quickly became clear that we could achieve much more together,” she says.

”Bayou brings deep expertise in the US foodservice market, manufacturing, and commercial execution. BettaF!sh brings European seaweed expertise, proprietary processing know-how, a strong consumer brand, and experience developing both ingredients and finished products.”

This will enable them to create a stronger platform with a broader product portfolio, expertise in two key markets, and a ”shared vision of where food needs to go”.

”Startups can push the boundaries, but transforming our food system also requires leadership from governments, industry, and retailers,” she says. ”We need change from the top as well as from the bottom.”