Cultivated Meat Outlook: 10 Leading CEOs Lay Out Their Challenges & Plans for 2026

Cultivated meat is at a critical juncture, with investment at a seven-year low and the closure of several pioneering startups. Now, some of the leading players speak to Green Queen about their plans for 2026, and the industry’s future.

“The cultivated protein sector is entering a more demanding phase, as capital is much more selective,” says Lou Cooperhouse, founder and CEO of US cultivated seafood startup BlueNalu.

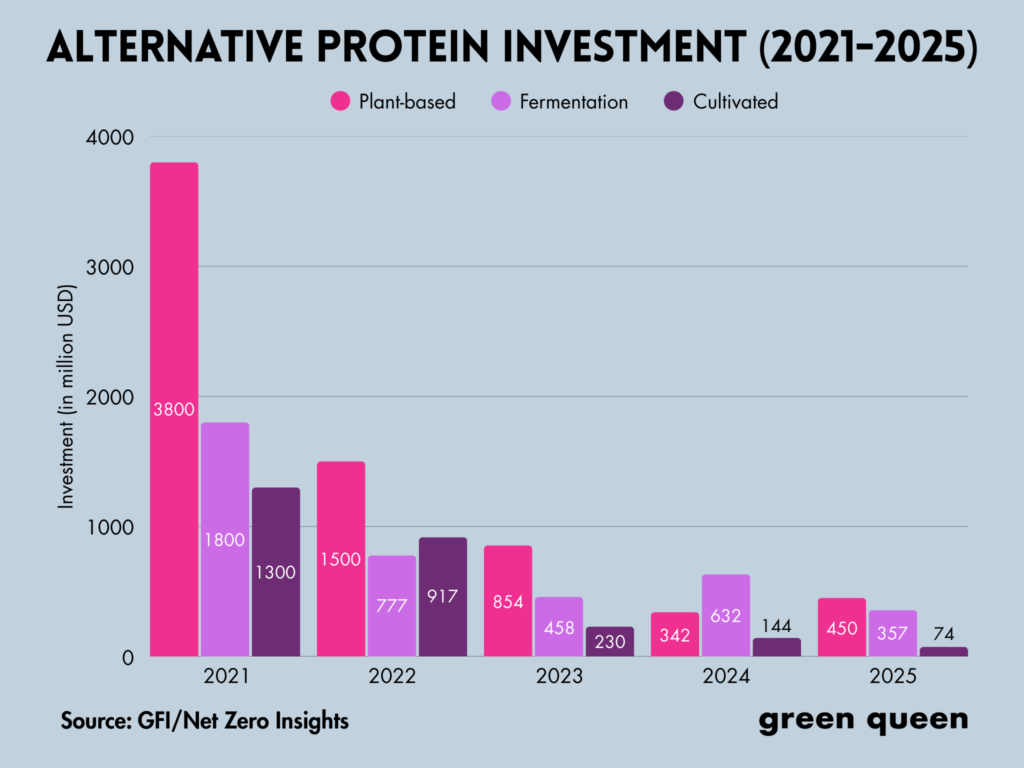

In 2021, at the height of its popularity, this sector pulled in $1.8B in funding, and its star had never been higher. Things, however, unravelled quickly. Last year, cultivated meat companies only managed to raise $74M – that’s a 96% decline in four years, and the lowest total since 2018.

These fundraising challenges caused the closure of some leading industry players, including Believer Meats (which had secured both FDA and USDA approval to sell cultivated chicken) and Meatable. Others, like Uncommon Bio and Upside Foods, either divested or diversified from cultivated meat to focus on the medtech and life sciences sector.

Investors have given cultivated meat companies a brutal reality check, but those still standing continue to be optimistic – if not bullish – about their prospects. The promise of the technology, they say, remains as strong as ever.

“The companies that will succeed are those that demonstrate culinary quality, a short-term pathway to both scalability and profitability, and products that can demonstrate a significant value proposition and market fit,” argues Cooperhouse.

He is one of 10 cultivated meat CEOs who spoke to Green Queen about their companies’ plans for 2026, and their outlook on the industry’s future.

“I see the defining work of this next chapter as moving cultivated meat out of the headlines and into people’s hands,” says Uma Valeti, co-founder and CEO of Upside Foods.

“We have spent years proving the fundamentals of science, safety, and regulatory pathways, which was a formidable and necessary stage in pioneering this field,” he adds. “Now, the measure of progress is executing on scale so that customers can experience and love these products.”

Funding and scale-up remain cultivated meat’s top barriers

“The biggest challenges facing the industry this year are scaling and funding, and the two are inseparable,” asserts Max Jamilly, co-founder and CEO of London-based Hoxton Farms, which is focusing on pork fat for hybrid meat.

He argues that the companies that recently shut down didn’t do so because the science failed, but because their business and manufacturing models didn’t translate to scalable, capital-efficient production in a tougher funding landscape.

“As a result, investors are rightly focused on manufacturing economics, regulatory realism and time to market, which is a healthy correction for the sector,” he says.

Didier Toubia, co-founder and CEO of Israeli cultivated beef maker Aleph Farms, concurs. He believes efficient scale-up and attracting the “right kind of capital” are the sector’s major battles.

“The industry has moved past its early hype cycle and is now judged on execution, risk management, and consumer relevance rather than vision alone,” he says.” Companies that succeed will be those that demonstrate the right product strategy, operational discipline, credible and transparent profitability pathways, and strong partnerships across the value chain.”

While political pressure and public perceptions do matter, Jamilly reiterates the importance of showing that you can make cultivated meat tasty, wallet-friendly, and at scale.

“The way forward is to design for scale from day one: focus on high-impact, low-inclusion ingredients, build cost-efficient bioprocesses and work closely with regulators and customers,” he suggests. “Companies that pair delicious products with feasible economics and a clear path to revenue will continue to attract capital and move the industry forward.”

Niya Gupta, co-founder and CEO of Fork & Good, believes scaling up in a cost-efficient manner requires both technological innovation and infrastructure development. “If you’re in food, you have to be pragmatic and operate lean,” she says.

Most cultivated meat companies are fundraising

Most of the companies Green Queen spoke to for this story explicitly stated that they are fundraising this year. “We are always evaluating opportunities to bring on strategic investors who align with our mission,” says Gupta. “In the current environment, capital needs to [be] focused on proving the path to revenue, particularly to support commercialisation, partner deployments, and licensing,” she adds.

Harsh Amin, co-founder and CEO of UK-based Ivy Farm Technologies, confirms his startup is raising capital to accelerate its scale-up and commercial launch. “We’re tantalisingly close to key cost-down and scale milestones – the inflexion point where cultivated meat moves from promising to commercially viable,” he says.

Combining “technical progress with disciplined commercial execution” will be the key to success for the industry, which needs investors “who understand that this is mission-critical infrastructure for the future food system, not a short-term bet.”

BlueNalu, which closed an $11M round in December, will also continue to raise money to prove the “marketability, scalability, and profitability of our business”. “Additional capital will support the next phase of the business, scaling production capacity, supporting commercialisation with partners, and advancing regulatory pathways in key markets over time,” says Cooperhouse.

Japan’s IntegriCulture, which broke even last year with a profit of $300,000, is expecting to close its next round of funding in March-April, followed by a second close in May-June. “The total amount is $3-4M, to be allocated for business development and sales efforts,” reveals founder and CEO Yuki Hanyu. “I could call this use of funds as ‘scaling’, but not in the sense of building bigger bioreactors.

Wildtype and Mission Barns, two startups that began selling their salmon and pork products in the US last year, respectively, say they’re raising money too. The latter’s CEO, Cecilia Chang, suggests its effort will be “focusing on scale-up and bringing our products to market with our partners”.

Aleph Farms secured $29M from a SAFE conversion and the first close of a new round in 2025, with further investment expected soon. “Given the sector’s shift towards capital discipline and fundamentals, we are focused on strategic capital that supports commercialisation and expansion through long-term partnerships and infrastructure-light models, rather than headline valuations,” says Toubia.

“Investors are increasingly valuing lean companies that can balance differentiated technology, regulatory preparedness, and clear profitability pathways supported by credible unit economic analysis,” he adds.

In China, Joes Future Food has also devised a financing plan for this year, following the construction of the country’s largest cultivated meat pilot plant.

Expectation, validation, demand and regulation: the other major challenges

“Funding is obviously a major challenge for the cultivated meat space right now, but we see that as downstream of a few more fundamental issues,” suggests Mission Barns’s Chang.

“The biggest challenges are demonstrating clear demand for cultivated meat and fat, and proving that we can achieve profitable unit economics at scale. If the industry can build stronger conviction around those two points, we believe capital will follow,” she says.

Fork & Good’s Gupta feels the real problem isn’t technology, but market validation: “The industry has yet to demonstrate the clear value proposition and corresponding willingness to pay of customers at scale. The way forward is to move away from ‘if we build it, they will come’ and more on commercial proof: paid partnerships, real offtakes, and integration into existing food supply chains.”

For some, expectation-setting is a more pressing issue. As a first-of-a-kind sector, some companies will succeed, and others will pivot or consolidate. “The risk is that individual setbacks are misread as systemic failure,” says Amin from Ivy Farm Technologies.

“Clear communication is critical. Cultivated meat is a long game, but it’s a necessary one. Global beef demand continues to rise – projected to increase by 10-15% by 2030, while land, water, and climate constraints tighten. The status quo simply doesn’t scale,” he outlines.

“For us, specifically, the challenges are regulatory timelines and a tougher funding environment. On the positive side, we’re consistently hitting taste and cost-down targets. The next step is getting real product into people’s hands through chefs’ menus and commercial partners who know how to excite consumers.”

Despite the obstacles being culture- and geography-specific, the root of it all is the limited availability of products on the market, according to IntegriCulture’s Hanyu.

“As long as cellular agriculture remains capex-intensive, this is very difficult to solve. To shrink the capex, we need lots of engineering R&D and rapid prototyping,” he says. “Then, soon, we would probably start seeing a competition over who has accumulated operational excellence the most.”

Ding Shijie, co-founder and CEO of Joes Future Food, believes that the most daunting challenge for companies in this space is survival. “Even if the regulations are passed, it does not mean that commercial sales can be carried out. To overcome this, I believe more cooperation is needed,” he says.

“On the one hand, enterprises themselves need to better refine their technologies and form competitive technical routes. On the other hand, the industry should share more of the know-how from the regulations and cooperate to establish concepts such as low-cost culture media, reactors, and factory designs, so as to truly promote the industry towards industrialisation.”

Which companies can sell cultivated meat so far?

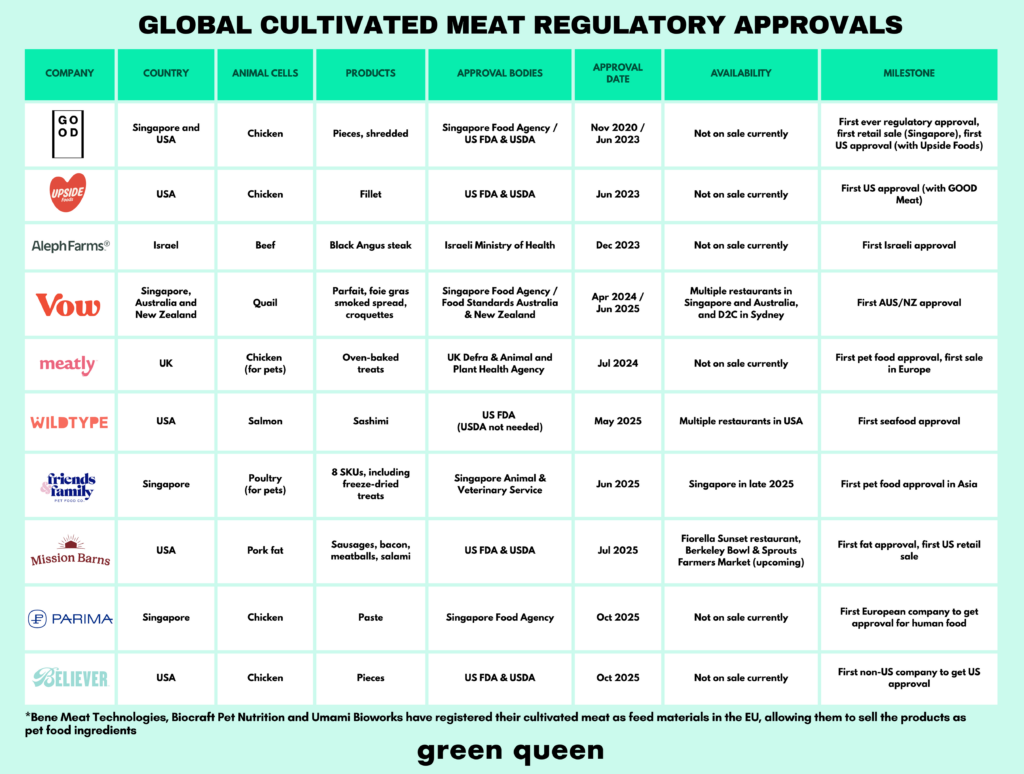

So far, 12 active companies have received some form of regulatory clearance to sell cultivated meat – for either humans or pets, spanning six countries plus the EU.

Eat Just’s Good Meat, Upside Foods, Wildtype, and Mission Barns can all sell their products in the US, while Good Meat, Vow, Parima, and Friends & Family Pet Food Co have received the green light in Singapore. Vow also has approval to sell in Australia and New Zealand, Aleph Farms in Israel, and Meatly in the UK.

Meanwhile, Bene Meat Technologies, Biocraft Pet Nutrition, and Umami Bioworks have all registered their cultivated meat products as feed materials in the EU, allowing them to sell their innovations as pet food ingredients.

Aleph Farms is also awaiting clearance in Singapore, Switzerland, the UK, and Thailand, and has the UAE and the EU in its sights too. Mission Barns “may prioritise additional international regulatory approvals”, but is currently focused on the US. And Wildtype says it will continue “to work with regulators in a number of countries to expand distribution”.

Will 2026 bring in more regulatory approvals for cultivated meat?

Many others are waiting in the wings. BlueNalu is “in the final stages of the FDA pre-market consultation process, which is required prior to commercial sale” in the US. It’s also engaging with regulators in Singapore and other Asia-Pacific nations, the UK, and the Middle East.

“Our approach is phased: entering the market, learning from early commercialisation, and expanding geographically as additional regulatory approvals are secured,” says CEO Cooperhouse. “Regulatory timelines ultimately rest with authorities, but we’ve prioritised transparency, data rigour, and constructive engagement throughout the process.”

Hoxton Farms has filed in Singapore, and as part of the UK’s cultivated meat sandbox programme, expects to submit its full dossier in its home country soon. “The sandbox has been extremely constructive and has helped clarify requirements well ahead of submission,” says Jamilly.

“We are planning filings in the US and selected Asian markets with established cultivated-meat regulatory frameworks, including Japan, Thailand, South Korea and potentially Hong Kong,” he outlines, suggesting that the focus is on jurisdictions that offer “clarity, collaboration and predictability”. “We currently sell our product to customers for R&D purposes, and expect to be in a position to sell commercially from early 2027.”

Its compatriot, Ivy Farm Technologies, has submitted dossiers in the US, the UK, and Singapore. “We recognise that regulators are under immense pressure to get this right, and we respect the rigour required to bring a truly novel food category to market safely,” its CEO, Amin, notes.

“At the same time, speed matters. Every year of delay increases the risk that well-intentioned, science-backed startups run out of capital before consumers ever get the chance to try the product. Continued collaboration between regulators and industry will be essential to ensure innovation reaches the market responsibly and in time.”

Fork & Good is actively engaged with regulators in markets with “clear regulatory pathways and strong commercial pull”. “We pursue regulatory approvals where we already see concrete customer demand. While regulatory timelines are inherently difficult to predict, we expect meaningful progress in select markets over the next 12–24 months,” says co-founder and COO Patricia Bubner.

In Asia, Joes Future Food expects to obtain approval in Singapore this year. “The plan is to complete the applications for Australia, the United States and Europe by 2026,” adds Shijie.

For IntegriCulture, cultivated meat products aren’t its main revenue focus – it is primarily spotlighting its cosmetics business – so regulation isn’t a critical issue. “Yet, it is still important, as our cell-ag infrastructure products need credibility and validation,” says Hanyu, who is eyeing approval for cultivated duck mainly as a validation for the firm’s process, materials and equipment.

“We are planning to submit a dossier right away for our Craft Essen, cell-cultured primary duck liver cells grown on edible scaffold in a packed bed bioreactor, using zero insulin, transferin, growth factors or anything that looks like biopharma when listed on a food label),” he adds. “We are also thinking of submitting in other jurisdictions.”

Collaboration is the name of the game

For several of the startups Green Queen interviewed, the chief focus for 2026 was deepening commercial partnerships.

“Developing infrastructure and operating lean don’t sound like they go hand in hand, which is why collaboration is no longer a nice-to-have; it’s a necessity,” explains Gupta from Fork & Good. “The companies with the best ecosystem of partners will have the best chance of pulling off the jump to commercialisation.”

It’s why the New Jersey startup will focus on fostering strategic partnerships, like its recent deal with Nutreco and Extracellular, which will “help us to get to a cost-efficient process at scale”, according to co-founder Gabor Forgacs.

The team is working to demonstrate “real market validation” for cultivated beef and pork. “That means converting our technology into repeatable commercial demand beyond the revenue-generating joint development and offtake arrangements we already have across the globe,” says Gupta.

Likewise, Hoxton Farms will focus on bolstering its commercial partnerships with food manufacturers globally, while improving its unit economics.

“2026-27 is when Hoxton Farms transitions into a scalable, revenue-generating business by embedding our product into real customer pipelines,” says Jamilly, its CEO. “We’re building on strong technical progress, a de-risked regulatory path and clear evidence of customer demand.”

For Ivy Farm Technologies, 2026 is a pivotal year on a commercial level. “Our priority is building deep commercial partnerships that translate our technology into products consumers genuinely want to eat,” says Amin.

“This year is about preparing to launch our cultivated beef expertly: ensuring taste, real cost, nutrition, safety, and storytelling align, so we build long-term trust with consumers and partners alike.”

Partnerships are a focus for Joes Future Food, too. “We will collaborate with some suppliers of growth medium raw materials to establish specific raw material standards for cultured meat,” says CEO Shijie. “We need to reduce our production cost to ¥100-500 per kg.”

At IntegriCulture, “normalisation” is the overarching goal for the year. Hanyu notes that the startup’s profitability was thanks to one-off factors like a government grant, it is aiming to turn a positive net profit without this by 2028: “Then we can say that we (and cellular agriculture) have reached real viability.”

Leading startups target cultivated meat launches in 2026

BlueNalu’s Cooperhouse highlights how the company’s primary goal for the year is “disciplined execution”. “That means entering the market with our cultivated bluefin tuna toro, and scaling production in a measured, capital-efficient way,” he says.

“In the near-term, we’ll be focused on finalising our US regulatory process, entering the market, and learning from our initial launch partners,” the CEO adds. The startup will also build on its consumer research (which shows strong receptivity to its tuna) with real-world product performance and acceptance data.

“We’ve also developed our plans for expanded commercialisation activities, and we will use our initial market learnings to support a thoughtful and meaningful business expansion. In parallel, we’re advancing regulatory pathways in additional key markets to enable thoughtful geographic expansion over time,” Cooperhouse states.

BlueNalu’s strategy echoes with Aleph Farms’s focus on “disciplined commercialisation”, based on years of production enhancement and product-fit validation via commercial agreements. “We now have built operational foundations needed towards profitable and sustainable growth through concrete regional partnerships and production frameworks,” says Toubia.

“That means executing our asset-light approach and strengthening regional engagement in markets like Southeast Asia, Switzerland, and beyond. It is about delivering on cultivated meat’s promise with realistic, lean and capital-efficient execution, informed by rigorous technical, market and economic validation. In short, building a successful and healthy business,” he adds.

“We are also actively looking at external growth opportunities, as we believe Aleph Farms could play the role of an aggregator in this maturing and consolidating ecosystem.”

Mission Barns is also doubling down on product launches with B2B partners, who will use its Mission Fat to create hybrid meat offerings. “In parallel, we’re focused on continuing to scale production and drive costs down, which is critical for making cultivated fat commercially viable across more use cases,” says Chang.

Wildtype co-founder and CEO Justin Kolbeck reveals that its salmon has been available for purchase every week” since its FDA approval in May. This year, the company has one primary goal: get its product on as many customer plates as possible.

“We’ve recently made a few major efficiency improvements and are ready to serve new customers. We expect to go through growing pains as we continue to scale up and reach new customer segments,” says Kolbeck.

Reflecting on the industry’s 2026 challenges, Upside Foods’s Valeti notes: “As the saying goes about sausage-making, the pioneering work isn’t always pretty; it requires tightened focus and some consolidation.

“This is the rollercoaster every transformative industry must ride as it moves from ‘Can it exist?’ to ‘Can it last?’. I’m more optimistic than ever, because we’ve crossed the threshold from science fiction to reality, and the next chapter is launching beloved products at scale.”

Vow and Parima declined to be interviewed at this time. Eat Just, Clever Carnivore, SuperMeat, Umami Bioworks, and Mosa Meat did not respond to Green Queen’s requests for comment.